‹ All Blogs

‹ All BlogsAutomated Loan Decisioning: Approve More Loans Without More Risk

Every chief lending officer has heard some version of the same argument: if we a...

The False Choice Between Approval Rate and Credit Quality

Every chief lending officer has heard some version of the same argument: if we approve more loans, we take on more risk. It sounds axiomatic. It feels prudent. And for institutions running rule-based underwriting built on a handful of variables from a credit report, it has historically been true.

But it is not a law of lending. It is a limitation of the tools.

The relationship between approval rate and credit quality is not fixed; it is a function of how accurately your decisioning system can distinguish between borrowers who will repay and borrowers who will not. When that distinction is made with a narrow, static scorecard that evaluates five variables at a single point in time, the only way to control for risk is to tighten the thresholds and tightening the thresholds means declining creditworthy members.

When that distinction is made with an AI model that evaluates hundreds of data dimensions in combination, identifies behavioral patterns that predict repayment across different economic conditions, and improves over time as new performance data is incorporated, the tradeoff changes. You can approve more qualified members because the system is better at identifying who they are not because you have relaxed your standards.

This is the promise of automated loan decisioning done correctly. This article explains the mechanisms behind it: how supervised AI delivers accuracy without black-box risk, how champion-challenger testing lets CLOs validate performance before deploying changes at scale, how backtesting protects against credit policy drift, and how all of it translates into higher look-to-book ratios and sustainable portfolio growth.

How Does Automated Loan Decisioning Increase Loan Approval Rates Safely?

The answer has four parts, each addressing a specific limitation of the manual underwriting and static rules-based systems that most credit unions are operating today.

Traditional underwriting relies primarily on bureau credit scores - a snapshot of credit history derived from a limited set of tradeline variables. This works well for borrowers with deep, established credit files. It systematically underestimates the creditworthiness of members who are thin-file, new-to-credit, or whose credit history does not fully reflect their current financial stability.

Consider the 28-year-old member who has been with the credit union for six years, maintains consistent deposit balances, has never had an overdraft, and pays rent and utilities on time every month. Her FICO score may be below the threshold that triggers a hard decline under a rules-based system not because she is a credit risk, but because her credit file is thin relative to the score's input requirements. A rules engine never sees the deposit history, the payment patterns, or the membership tenure. It declines her based on the absence of evidence, not on evidence of risk.

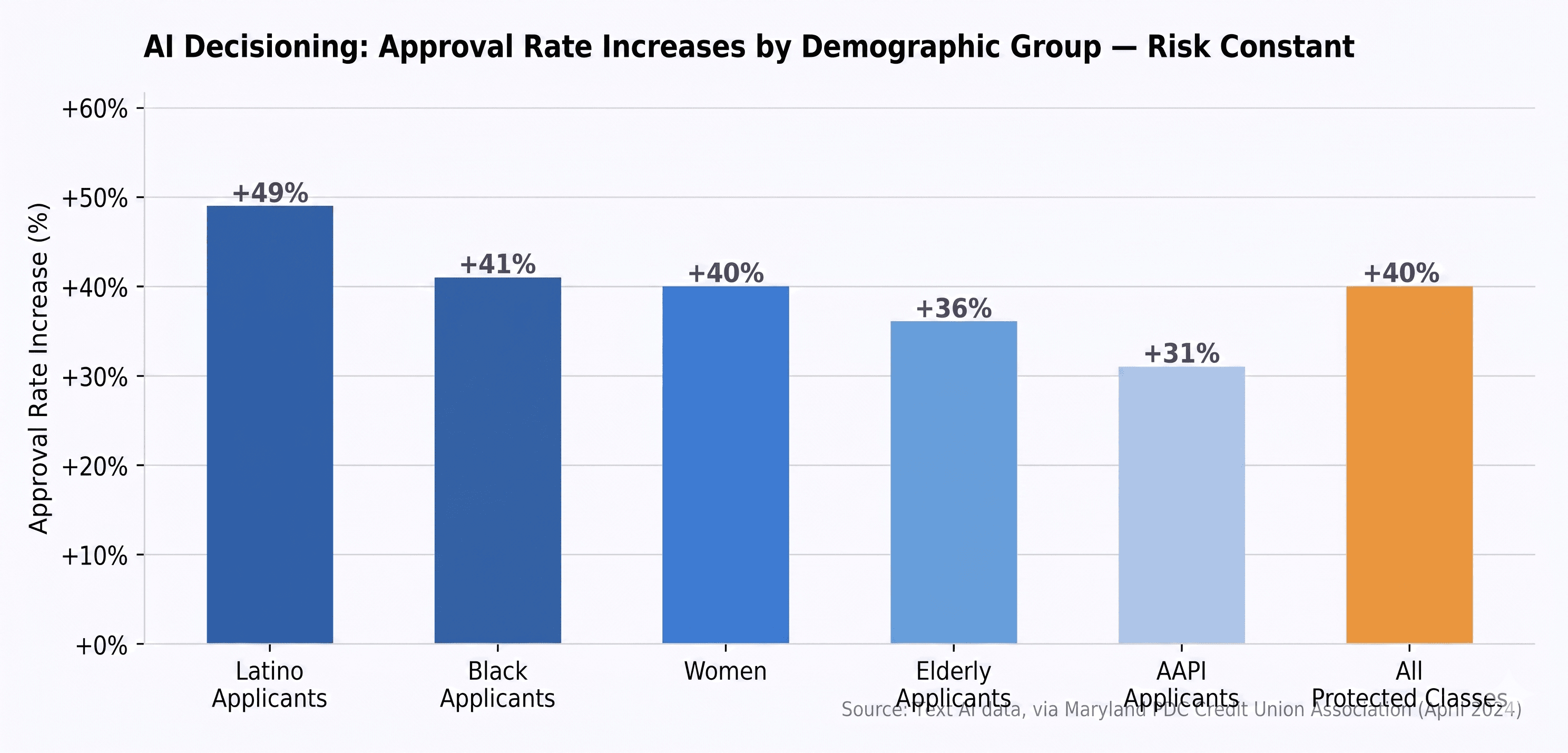

An AI decisioning model with access to alternative data sources and the credit union's own account relationship data sees a different picture entirely and makes a different decision. AI-based scoring models have demonstrated approval rate increases of 20 to 30 percent for previously unscorable borrowers without a corresponding increase in default rates. Those are not riskier loans. They are better-analyzed loans.

Manual underwriting introduces variability that cuts in both directions. Experienced underwriters working from the same policy may reach different decisions on the same application depending on when in their day they review it, how much of their queue they have remaining, and which compensating factors they weight most heavily. This inconsistency means some borderline applications that should be approved are declined and some that should be declined are approved.

Automated decisioning eliminates this variance. The same credit policy, applied consistently through a configurable rules engine, evaluates every application by the same logic every time — at 2pm on a Tuesday and at 11pm on a Saturday in an indirect lending channel. Configuring your risk appetite correctly is what determines the quality outcome. Once configured, the system enforces it with a precision no manual process can match.

Credit unions operating automated decisioning consistently report that delinquencies either remain flat or improve after implementation because the system catches the inconsistencies and errors that manual review misses, not because the risk tolerance has changed.

Rules-based underwriting evaluates risk dimensions independently. If DTI is below 43%, that condition passes. If the credit score is above 640, that condition passes. Each variable is assessed in isolation against a threshold, with no evaluation of how variables interact.

AI models evaluate variables in combination which is how credit risk actually works in the real world. A borrower with a 680 FICO score, strong income, and minimal tradeline history is a different risk profile than a borrower with a 680 FICO score, moderate income, and three recent derogatory marks. The scores are the same; the risk is not. An AI model trained on historical performance data learns to distinguish these profiles with accuracy that a static threshold cannot approach.

This bidirectional accuracy is what makes expanded approval rates risk-neutral: the same model that approves more qualified thin-file borrowers also declines more high-risk borrowers who would have slipped through rules-based thresholds precisely because no single variable tripped a hard floor.

Lending risk is not static. Economic conditions shift. Delinquency patterns change. New member segments arrive with different risk profiles than the portfolio the model was trained on. A credit policy that was correctly calibrated in a low-rate environment may over-approve in a rising-rate environment where debt service burden changes materially.

Automated decisioning platforms with configurable policy controls allow CLOs and risk teams to tighten or relax specific underwriting parameters in real time adjusting DTI thresholds, credit score floors, or product-specific risk tiers without waiting for an IT release cycle or reprogramming a system that is not designed to change. When the NCUA identifies new supervisory priorities around credit risk, when your portfolio analytics surface an emerging delinquency trend in a specific product tier, or when the macro environment shifts, your decisioning engine should respond at the same speed. A static system cannot do this.

What Is Supervised AI in Lending and Why Is It Safer Than Autonomous Models?

Not all AI decisioning is equivalent. The architecture of how humans and AI interact in the decisioning workflow has significant implications for risk management, regulatory compliance, and the credit union's ability to understand, audit, and correct its own lending decisions.

In a supervised AI model for lending, the machine learning model is trained on historical loan performance data with clear outcome labels a loan either performed or it did not under direct human oversight. Risk teams review model inputs, validate outputs, audit for bias, and can adjust the policy environment within which the model operates. The model's role is to generate risk assessments and credit recommendations; the credit policy that determines what happens with those assessments is set and controlled by humans.

This is meaningfully different from an autonomous or "black-box" model that makes final credit decisions with no human governance touchpoints where the model's internal logic is opaque, changes to decisioning behavior go undetected, and the institution cannot explain how a given decision was made.

The Federal Reserve and OCC's SR 11-7 guidance on Model Risk Management, the foundational regulatory framework for AI governance in banking requires that financial institutions validate their models, understand their limitations, and monitor their performance continuously. NCUA has reinforced this expectation through its AI Compliance Plan, which hired three AI officers for 2025-2026 specifically to assess AI governance in credit unions. What regulators expect is not the absence of AI in lending, it is the presence of human oversight, explainability, and validation frameworks around AI in lending.

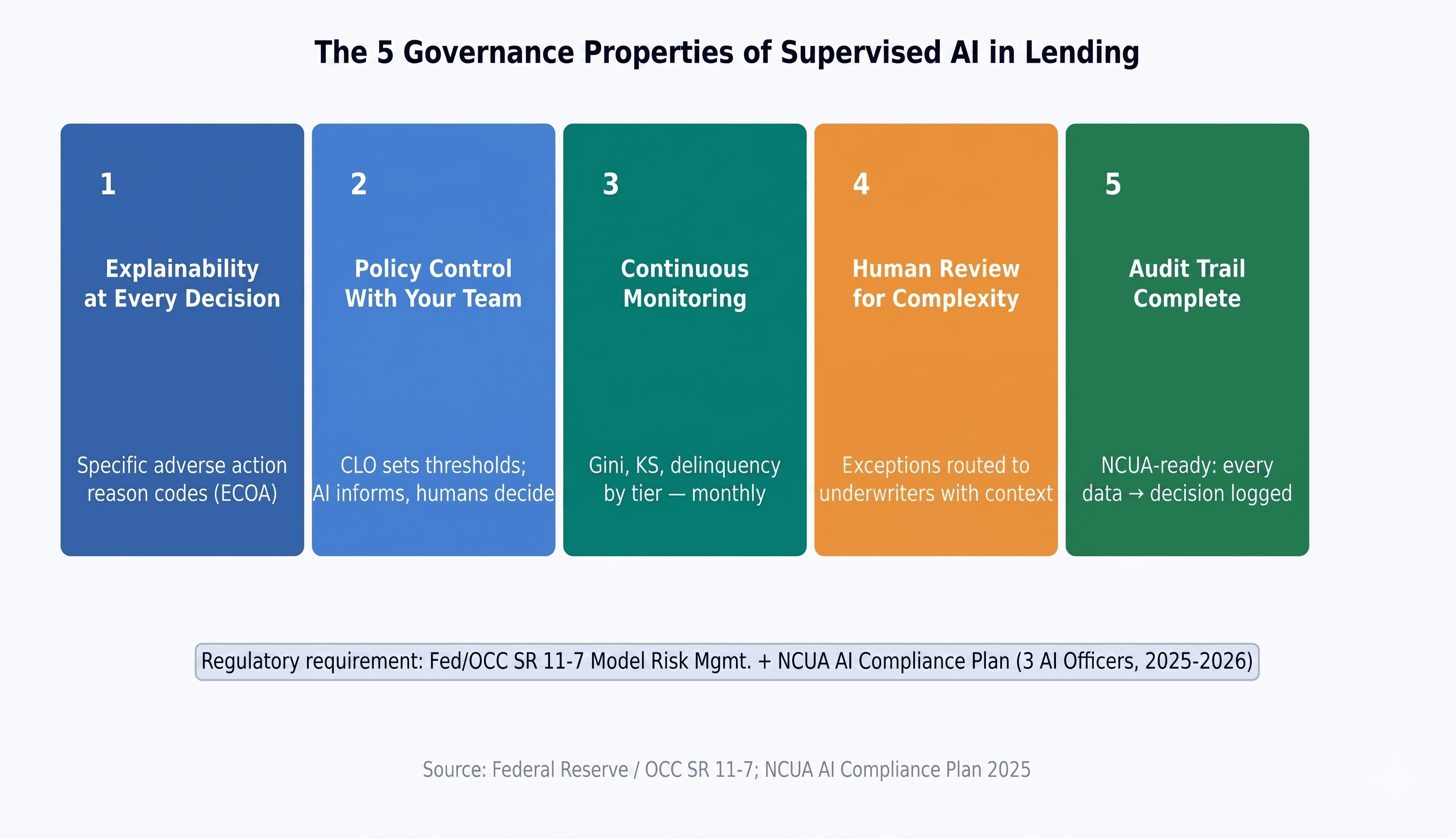

Why Supervised AI Is Safer: The Five Governance Properties

Explainability at every decision. In a supervised AI environment, every credit decision produces human-readable reason codes that trace back to the specific input factors that drove the outcome. Loan officers can review the AI's assessment and understand why it recommended an approval or a decline. Compliance teams can audit adverse action notices against the actual decision drivers. Examiners can follow the logic from application through decision without encountering a step that is invisible to human review.

Policy control remains with your team. The AI model generates risk predictions. The credit policy, the threshold above which an application is approved, the product tiers within which different risk levels are eligible, the compensating factors that allow exceptions is set by your CLO and risk team. When your board adjusts risk appetite in response to economic conditions, the policy change is configured in the decisioning engine by your team. The model's risk predictions do not change your policy; they inform it.

Model performance is monitored continuously. Supervised AI environments include ongoing model monitoring, tracking whether the model's risk predictions are performing as expected against actual loan outcomes, whether approval rates are drifting from policy intent, or whether disparate impact patterns are emerging across protected classes. When the model begins to drift from expected performance, the monitoring system surfaces it before it becomes a portfolio problem.

Human review is preserved for complexity. Supervised AI routes straightforward, in-policy applications to auto-decision. Complex applications exceptions, high-value relationships, unusual income profiles, borderline cases are routed to human underwriters with the AI's risk assessment as context. Underwriters are not replaced; they are elevated from data gatherers to judgment appliers, with better information than they had before.

Audit trails are complete and defensible. Every decision made in a supervised AI environment is logged: what data was received, which model evaluated it, what risk score was produced, which policy rule determined the outcome, and what adverse action codes were generated. When an examiner asks why a specific application was denied eighteen months ago, the answer is in the system.

Autonomous models that make final decisions without these governance properties invert each of these protections. The risk of undocumented, opaque, and ungoverned AI in credit decisions is not theoretical; regulators globally have imposed significant penalties on institutions that deployed decisioning systems they could not explain or audit.

How Do Credit Unions Use Champion-Challenger Testing to Improve Loan Decisioning?

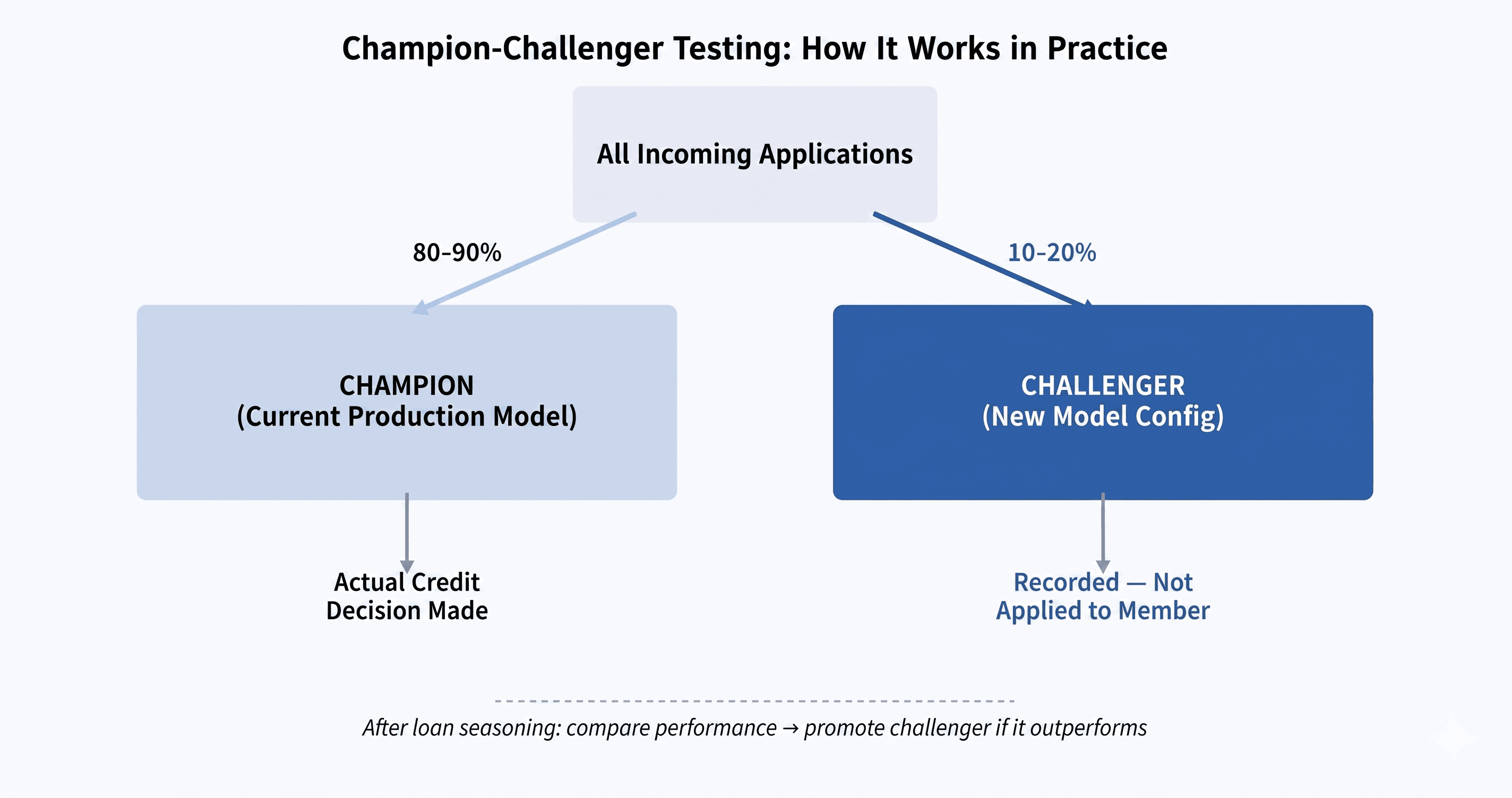

Champion-challenger testing is the gold-standard methodology for improving a credit decisioning model while protecting the credit union from the risk of deploying an unvalidated change at full production scale.

In a champion-challenger framework, the current production decisioning model the "champion" continues to process the majority of applications as it normally would. A new model configuration, the "challenger" processes a defined subset of applications simultaneously. Both models evaluate the same applications, but only the champion's decisions are actually used for lending. The challenger's decisions are recorded but do not affect applicants.

Over the observation period, the credit union accumulates performance data on both models: approval rates, risk stratification accuracy, disparate impact patterns, and as the applications season into actual loan performance - default rates and delinquency patterns. When the challenger has demonstrated consistent improvement over the champion across a statistically meaningful sample, the challenger can be promoted to champion with confidence grounded in actual performance data, not theoretical modeling.

The practical value of champion-challenger testing for chief lending officers is that it eliminates the "big bang" risk of decisioning model changes. Without this framework, improving your decisioning system requires a choice between keeping the current model indefinitely (no improvement) or replacing it all at once and discovering its real-world performance after the fact (uncontrolled risk).

Champion-challenger gives CLOs a third path: continuous improvement under controlled conditions, with performance data accumulating before any change affects full production volume. When the credit union's portfolio analytics surface an opportunity in a segment where the current model appears to be over-declining creditworthy borrowers, or where delinquency is higher than the model predicted - the challenger framework allows the hypothesis to be tested at limited exposure before it becomes policy.

For NCUA examinations, challenger data also provides concrete validation evidence: the institution can demonstrate that its model changes are based on head-to-head performance comparison, not intuition or vendor recommendation.

The mechanics require a decisioning platform that supports parallel model evaluation not all systems do. Key implementation questions for CLOs evaluating their decisioning infrastructure:

Can the system route a defined percentage of applications to a challenger model automatically? The allocation should be configurable by product type, member segment, or application characteristic, not a blunt instrument that applies uniformly across all applications.

Is the challenger evaluation truly independent from the champion's decision? The challenger should evaluate applications based solely on its own inputs and logic, not in a way that is influenced by the champion's output.

How does the system track challenger performance over time? Approval rate comparison alone is insufficient. The meaningful metrics are risk-adjusted approval accuracy (did the challenger make better distinctions between good and bad risk?) and ultimate loan performance (did applications the challenger would have approved perform as expected?).

What is the promotion process? Clearly defined criteria for when a challenger becomes the new champion and governance approval that the criteria have been met creates the accountability structure that regulators expect.

While champion-challenger testing evaluates a new model configuration against live applications going forward, backtesting evaluates how a model would have performed on historical applications applications that were already made, decided, and whose outcomes are already known.

A backtesting exercise takes a defined historical population of loan applications including both approved loans whose performance is now observed and declined applications whose performance cannot be directly observed and runs them through a proposed new model configuration. The model's decisions are then compared against the actual outcomes of the applications it saw.

For approved loans, the comparison is direct: did the model's risk score accurately predict which loans performed and which did not? A model with strong discrimination accuracy should assign lower risk scores to applications that subsequently defaulted and higher scores to applications that performed well. The Gini Index and Kolmogorov-Smirnov (KS) score are the standard metrics for measuring this discrimination accuracy.

For declined applications, backtesting can assess whether the proposed model would have approved a population that the current model declined, and using statistical approximations of what their performance would have been estimated whether those additional approvals would have been additive to portfolio quality or detrimental.

It catches model deterioration before it affects the portfolio. Models trained in one economic environment may perform differently in another. A backtesting program that runs monthly or quarterly against recent application cohorts can detect when a model's discrimination accuracy is deteriorating, its Gini coefficient declining, its KS score weakening before the deterioration becomes visible as rising delinquency in the portfolio. This early warning function is what SR 11-7 means when it requires continuous model monitoring rather than one-time validation.

It provides an honest baseline for new model comparisons. When a vendor proposes a new decisioning model, the first question a CLO should ask is: how does this model perform on our own historical data? Running the proposed model against the credit union's actual historical application population - with known outcomes - is the only way to evaluate whether the vendor's performance claims hold up in the institution's specific lending environment. Generic model accuracy metrics are not a substitute for this.

It supports stress testing for economic scenarios. Backtesting against application cohorts from periods of economic stress - rising delinquency environments, rate shock periods provides evidence of how the model would perform in conditions different from the training environment. Since most AI models were developed and trained during relatively benign credit conditions, stress-period backtesting is the validation method that most directly addresses the risk of model underperformance in a downturn.

It creates defensible documentation for examinations. When NCUA examiners review the credit union's model risk management practices, backtesting documentation population definition, methodology, performance metrics, frequency of testing is the evidence that the institution is managing its models with the rigor regulators expect. An automated decisioning system without a backtesting program is a system whose performance is assumed rather than validated.

How Does Automated Decisioning Help Credit Unions Increase Look-to-Book Ratios?

The look-to-book ratio, the percentage of loan offers or approvals that actually result in a funded loan is one of the most direct measures of decisioning efficiency and member experience quality. It captures not just whether good decisions are being made, but whether those decisions are being delivered in a way that members act on before going elsewhere.

The most immediate driver of look-to-book ratio improvement through automation is speed. When a member applies for an auto loan through a dealership and receives a decision in under 60 seconds, they are still at the dealership. The dealer's ability to present the credit union's approval instantly before the member has time to check their phone for a competing offer is directly tied to the credit union's ability to deliver a real-time automated decision.

Gesa Credit Union's experience quantifies this relationship directly. The credit union's average look-to-book ratio sat at approximately 60 percent before automation. After implementing automated decisioning for auto loans, that ratio climbed to 90 to 95 percent. The loans being approved were not dramatically different. The members were not more committed to the credit union. The change was speed: the approval arrived while the member was still in the purchase moment, before the competitive window closed.

This pattern repeats across credit union implementations. The application that gets a decision in 30 seconds converts at a meaningfully higher rate than the application that gets a decision in 48 hours because in 48 hours, the member has already closed a loan with a faster competitor who got there first.

Look-to-book ratios are also affected by the quality of approvals, not just their speed. When approvals are made with inaccurate risk assessments approving applications at terms that do not reflect the actual risk profile the approved member may not accept the offer because the rate or terms are not competitive with what a more accurate model would have offered.

AI decisioning that produces better risk stratification allows the credit union to price credit more accurately: lower risk borrowers receive more competitive terms, higher risk borrowers receive terms calibrated to their profile. When a low-risk member receives an offer priced appropriately for their actual risk, acceptance rates improve because the offer is genuinely competitive. Accuracy and rate competitiveness are connected through the same mechanism: better risk identification.

Look-to-book ratios in modern lending are also a function of channel completeness. A member who applies on mobile, receives a tentative approval, and then faces friction completing the loan because the approval has not been carried through to the e-signature platform or the core system booking process will abandon even with a strong offer in hand.

Automated decisioning that is connected end-to-end from initial decision through document generation, e-signature, and core system update removes the handoffs and waiting periods that introduce abandonment risk between the decision moment and the funded loan. This integration is what makes the look-to-book improvement operational rather than theoretical.

The Risk Governance Framework: What CLOs Should Require

For chief lending officers evaluating or upgrading their automated decisioning infrastructure, the technical capabilities above only deliver sustainable value within a governance framework that treats AI decisioning with the rigor it requires. Here is what that framework should include:

Model validation before production. Any new decisioning model including updates to an existing model should be validated against the credit union's own historical data before deployment. Third-party validation is preferred for material model changes.

Continuous performance monitoring. Approval rates, auto-decisioning rates, risk tier distribution, delinquency by approval tier, and disparate impact metrics should be reviewed at least monthly. Significant deviations from expected ranges should trigger risk team review before they escalate.

Documented override controls. When a loan officer overrides an automated decision approving an application the model declined, or declining one it approved the override should be logged with a reason code. Override patterns over time reveal whether underwriting judgment is systematically diverging from model output, which is often the first signal of either model deterioration or underwriting culture misalignment.

Annual model review. At minimum annually, the decisioning model should be evaluated against its validation benchmarks Gini, KS, approval accuracy by risk tier and against the business outcomes the credit union cares about: loan volume, delinquency rate, look-to-book ratio, and NCUA examination results.

Board-level risk appetite articulation. The automated decisioning engine reflects the credit union's credit policy. That policy should be explicitly approved by the board including the auto-decision tiers, the referral thresholds, and the parameters that define each so that leadership accountability for the decisioning environment is clear and documented.

How Algebrik One Delivers Safe, High-Performance Automated Decisioning

Algebrik One's AI Decision Engine is designed for credit unions that want to approve more qualified members and hold portfolio risk steady without the governance trade-offs that come from black-box, vendor-controlled decisioning models.

Supervised AI with lender-controlled policy. The Algebrik Decision Engine generates risk assessments using AI models, but credit union lending teams configure the policy environment that acts on those assessments. DTI thresholds, credit score floors, product-specific approval tiers, and exception routing rules are set and adjustable by your CLO no engineering required. When economic conditions shift or board-approved risk appetite changes, the policy responds in real time.

Scienaptic AI integration for deeper risk intelligence. Through Algebrik's partnership with Scienaptic AI whose platform has processed over 3 million credit decisions monthly across 150+ credit unions, with 100% of clients passing NCUA audits credit unions accessing Algebrik One gain AI decisioning signals validated through deep credit risk expertise and rigorous disparate impact analysis. Scienaptic's models provide rich, diverse adverse action reasons and comprehensive documentation on model logic, robustness, and limitations the documentation framework that NCUA examiners look for.

Portfolio analytics for continuous monitoring. Algebrik's Portfolio Analytics module surfaces real-time visibility into approval rates, auto-decisioning rates, risk tier distribution, and portfolio performance metrics giving risk teams the data they need to detect model drift, identify policy misalignment, and validate that decisioning performance is tracking against expectation before variances become examination findings.

End-to-end integration for look-to-book results. Algebrik One connects the Decision Engine through Document Processing, Borrower Communication, and core system integration in a single unified workflow so that an AI-generated approval at 2pm can translate to a funded loan before 5pm, not three days later when the member has already moved on.

J.D. Power valuation data for auto lending accuracy. For credit unions operating auto lending programs, Algebrik One's integration with J.D. Power real-time vehicle valuation data ensures that collateral values used in decisioning reflect actual market conditions improving the accuracy of LTV calculations and reducing the risk of collateral valuation errors in the approval decision.

Frequently Asked Questions

How does automated loan decisioning increase loan approval rates safely?

Automated decisioning increases approval rates safely by giving the decisioning system access to a broader set of data inputs including alternative credit data, trended bureau behavior, and income verification that identify creditworthy borrowers who would have been declined by static, narrow rules-based underwriting. The safety comes from AI model accuracy: the same model that approves more qualified thin-file borrowers also declines more high-risk applicants who slip through threshold-based rules. When configured to the credit union's specific risk policy, automated decisioning can increase approval rates while holding delinquency flat or improving it because the system makes better distinctions between good and bad risk across the full applicant population.

What is supervised AI in lending and why is it safer than autonomous models?

How do credit unions use champion-challenger testing to improve loan decisioning?

What is backtesting in loan decisioning and how does it reduce credit risk?

How does automated decisioning help credit unions increase look-to-book ratios?

Ready to get started?

More Blogs

Blog

Computerized Loan Origination: How Technology Transformed Lending

Blog

Loan Origination System Requirements: A Checklist Before You Buy

Blog

Consumer Finance Systems: Why Unified Platforms Win Over Fragmented Stacks