‹ All Blogs

‹ All BlogsWhat are Loan Decisioning Softwares and Why Do they Matter?

Everything in a loan application leads to one moment: the credit decision. Incom...

The Decision Is the Bottleneck

Everything in a loan application leads to one moment: the credit decision. Income has been verified. Identity has been confirmed. Documents have been collected. And then nothing. The file sits in a queue, waiting for an underwriter who is already working through twenty other applications, each requiring the same judgment, the same data review, the same human time.

This is the bottleneck that loan decisioning software is built to eliminate not by removing human judgment from lending, but by ensuring that human judgment is applied only where it actually adds value, and that the rest of the pipeline moves at the speed members now expect.

For credit and risk officers, lending VPs, and CLOs at credit unions, understanding what loan decisioning software actually does and what separates a rules engine from a genuine AI decisioning system is no longer an academic question. It is a strategic one. The institutions that get this right are processing loan applications at scale, approving more qualified members, holding risk exposure constant, and funding loans the same day they are applied for. The institutions that have not made this shift are watching those members leave.

This article explains what loan decisioning software is, how it works, what it processes, how fast it operates, and what compliance obligations shape how it must behave with specific attention to what credit union leaders need to understand before evaluating or upgrading their decisioning infrastructure.

What Is Loan Decisioning Software and How Does It Automate Credit Decisions?

Loan decisioning software is a technology system that evaluates a loan application against a set of creditworthiness criteria and returns a credit decision to approve, deny, or refer to manual review without requiring a human underwriter to process each file individually.

At its most basic, loan decisioning software takes structured inputs (application data, bureau reports, income verification), applies a set of evaluation logic (credit policy rules, scoring models, or AI models), and produces an output (a decision plus the reason codes that support it). The automation lies in the speed and consistency with which this evaluation can happen - rather than the elimination of the underlying logic that your Credit Union or Bank has developed over years of lending experience.

There are three primary architectures for how that evaluation logic works, and each has meaningfully different implications for speed, accuracy, compliance, and flexibility:

- Rules-based engines evaluate applications against a fixed set of conditions: credit score thresholds, debt-to-income ratios, loan-to-value limits, employment tenure requirements. If an application satisfies all conditions, it is approved. If it fails any condition, it is denied or referred. Rules-based engines are transparent, auditable, and easy to configure but they are static. They apply the same logic to every application regardless of context, and they can only incorporate data dimensions that were anticipated when the rules were written.

- Scorecard models assign weighted point values to individual borrower attributes and produce a composite credit score that maps to a decision tier. Classic FICO scoring is a scorecard model. Scorecards are more nuanced than binary rules and have a long track record in regulatory compliance but like rules engines, they are static by design and are limited to the variables included in the model.

- AI and machine learning models evaluate applications dynamically, using statistical models trained on historical loan performance data to identify patterns that predict repayment behavior. Rather than testing a fixed list of conditions, AI models weight hundreds or thousands of data points in combination and produce risk assessments that improve in accuracy over time as the model learns from new data. When built correctly with explainability tools embedded at the decision layer, AI models can produce the specific, human-readable reason codes that ECOA and FCRA require.

In practice, modern loan decisioning software typically operates as a layered combination of all three: rules-based logic for hard policy boundaries (maximum DTI, minimum membership requirements), scorecards or AI models for risk stratification within those boundaries, and explainability frameworks at the output layer to ensure every decision can be communicated to the applicant and defended to a regulator.

What Is the Difference Between a Rules-Based Loan Decision Engine and an AI Model?

This is a longstanding question that credit and risk officers most commonly need to answer when evaluating decisioning infrastructure and it is one where precision matters, because the practical differences between a rules engine and an AI model affect how your institution lends, how quickly it adapts, and how it manages compliance risk.

A rules-based decision engine applies an explicit set of conditions your team has written. "If credit score is below 620, deny." "If DTI exceeds 45%, refer." "If the applicant has been a member for less than 90 days, require manual review." Every decision can be traced directly to a rule, which makes the system fully transparent and easy to audit.

The operational strength of rules-based engines is also their limitation: they can only make the decisions your team anticipated when writing the rules. When lending conditions change economic shifts, new borrower segments, emerging fraud patterns, etc, the rules have to be updated manually, which is a slow process that lags behind market reality. Rules engines also have a natural ceiling on accuracy: they evaluate each risk dimension independently rather than in combination, missing the interaction effects that predict default risk more accurately.

When rules engines work well: Hard policy cutoffs, compliance guardrails, simple loan products with predictable borrower profiles, and institutions that prioritize transparency and simplicity over predictive accuracy.

AI and Machine Learning Models: Adaptive, Predictive, and Explainability-Dependent

An AI decisioning model does not evaluate a checklist of conditions, it calculates the probability that a given borrower, with a given combination of attributes, will repay a loan of a given type under current market conditions. The model is trained on historical loan performance data and updated as new outcomes are observed, which means it improves over time rather than requiring manual rule updates when conditions shift.

The practical advantages are significant. AI models can incorporate far more data dimensions than rules engines including alternative data sources that rules engines typically cannot use and they evaluate those dimensions in combination rather than independently. This produces more accurate risk stratification: more qualified members who would have been denied under rigid rules get approved, and riskier applications that would have slipped through rules-based thresholds are flagged for review.

The compliance implication is critical and cannot be overstated. The CFPB has explicitly stated in Circular 2022-03 and Circular 2023-03 that ECOA adverse action requirements apply to AI-driven decisions exactly as they apply to rules-based decisions. A model that cannot produce specific, principal reasons why a particular application was denied reasons that accurately reflect the actual decision drivers is not compliant, regardless of how accurate its risk predictions are. This means AI decisioning systems must be paired with explainability infrastructure typically SHAP (Shapley Additive Explanations) values or equivalent attribution methods that trace each decision back to the specific input features that drove it and translate those features into human-readable adverse action reason codes.

A black-box AI model one that produces accurate predictions but cannot explain how creates the kind of audit exposure that most credit union compliance teams will not accept, and should not.

When AI models work well: Institutions with sufficient historical loan performance data to train reliable models, diverse member populations with varied credit profiles (including thin-file borrowers), and high-volume lending environments where decision accuracy translates directly to portfolio performance.

The Hybrid Reality: Where Most Institutions Should Land

The binary between rules engines and AI models is a false choice in practice. Most modern loan decisioning platforms operate as hybrid systems: rules-based hard floors define the absolute policy boundaries within which the AI model operates, and explainability tools at the output layer ensure every decision regardless of how it was generated can be communicated in terms that satisfy ECOA, FCRA, and the member on the other end of the denial notice.

The critical distinction for credit union buyers is not "rules-based or AI" ; it is whether the decisioning system produces outcomes that are both accurate and explainable, configurable by your team without engineering support, and integrated tightly enough with your LOS that decisions surface where lending staff actually work.

What Data Inputs Does Loan Decisioning Software Use to Approve or Deny Applications?

The quality of a credit decision is restricted by the quality and breadth of the data the decisioning system can access. This is where the gap between older and modern decisioning systems is widest - not in the logic they apply, but in what they are actually evaluating.

Legacy decisioning systems, and many rules engines still in production today, evaluate a relatively narrow set of variables:

Bureau credit data: the three-bureau credit report, including FICO score, payment history, outstanding balances, derogatory marks, credit utilization, account age, and public records. This is the foundational data source for virtually all consumer credit decisions.

Application data: borrower-reported income, employment status, loan amount requested, loan purpose, and term preferences.

Collateral data: for secured loans, the make, model, year, and estimated value of the asset being pledged.

These inputs were sufficient when they were the only scalable data sources available. They remain essential inputs for any decisioning system. But they leave significant predictive signal on the table and they systematically disadvantage creditworthy borrowers who do not have deep credit file histories.

Modern loan decisioning software supplements traditional bureau data with a richer set of inputs that materially improve decision accuracy:

Trended credit data evaluates how a borrower's credit behavior has evolved over time - whether balances are trending up or down, whether payment behavior has improved or deteriorated - rather than treating credit history as a static snapshot. This temporal dimension significantly improves default prediction accuracy.

Income and employment verification data draws on direct payroll data integrations (services like The Work Number, Plaid, MX) that provide real-time, source-verified income rather than relying on self-reported figures. For borrowers with variable income, cash flow analysis from bank transaction data provides a more accurate picture of actual repayment capacity than a W-2 snapshot.

Alternative credit data includes payment history for non-credit obligations - rent, utilities, subscriptions, telecom bills - that do not appear in traditional credit bureau files. For thin-file members particularly younger borrowers and recent immigrants with limited credit history alternative data is often the difference between an accurate credit assessment and a denial based on data absence rather than credit risk.

Fraud and identity signals include device fingerprinting, behavioral biometrics, identity document authentication, and watchlist screening. These inputs are evaluated not for creditworthiness but for application integrity flagging potential synthetic identities, application stacking, and misrepresentation before they affect the credit decision.

Property and collateral valuation data for auto loans draws on real-time vehicle valuation services (such as J.D. Power, which Algebrik One integrates with) to ensure that collateral values are accurate at the time of decision rather than relying on manual appraisals or outdated book values.

Portfolio and relationship data from the credit union's own systems existing account history, tenure, deposit behavior, prior loan performance provides signals about member creditworthiness that no external data source can replicate. Credit unions that fail to use this data in decisioning are leaving their most important competitive advantage unutilized.

The architecture of a modern AI lending decisioning system simultaneously queries all of these sources in parallel the moment an application is submitted and returns enriched, integrated data to the decisioning model in a matter of seconds, not the hours or days that sequential manual data gathering once required.

How Does Automated Loan Decisioning Ensure FCRA and ECOA Compliance?

Compliance is where the business case for loan decisioning software meets its most important constraint and where credit and risk officers should demand the most specificity from vendors. Compliance obligations for automated credit decisions are not aspirational guidelines; they are enforceable requirements with material regulatory and legal consequences for violations.

The Equal Credit Opportunity Act and Regulation B (12 CFR Part 1002) require written notification within 30 days of adverse action, identifying specific, principal reasons. The CFPB explicitly confirmed in Circular 2022-03 and Circular 2023-03 that this requirement applies to AI-driven decisions exactly as to human underwriters. A reference to a model score or algorithm is insufficient. The decision factors must be specific, in plain language, regardless of model complexity.

For credit union lending operations, this means that loan decisioning software must be evaluated not only on the accuracy of its decisions, but on the quality of its adverse action reason code generation. A system that produces accurate risk predictions but cannot trace those predictions back to specific, explainable input factors is a system that exposes the institution to regulatory risk every time it generates a denial.

The most technically rigorous approach to compliant AI explainability uses SHAP values, a mathematical framework that attributes each decision to the specific features that contributed to it, proportionally to their influence. SHAP-based adverse action codes are both accurate (they reflect what the model actually evaluated) and specific (they identify the actual factors, not generic categories). Compliant AI decisioning systems should be able to produce adverse action reason codes at this level of specificity automatically not as a manual override.

The Fair Credit Reporting Act adds a parallel set of obligations when adverse action is based in whole or in part on information from a consumer reporting agency. The adverse action notice must identify the CRA that provided the consumer report, include the CRA's contact information, disclose the credit score used, and identify the four factors that most negatively impacted that score.

In a modern decisioning system that queries multiple data sources simultaneously, compliance requires that the system track which specific inputs contributed to the adverse outcome credit report, income verification service, alternative data provider so that the appropriate FCRA disclosures can be generated automatically rather than manually assembled.

Automated decisioning systems can inadvertently encode demographic bias if training data reflects historical patterns that disadvantaged protected classes. Compliant AI systems include continuous disparate impact monitoring - tracking approval and denial rates across protected classes and surfacing anomalies for human review before they become regulatory findings.

Compliant AI decisioning systems include continuous disparate impact monitoring tracking approval and denial rates across race, gender, national origin, age, and other protected classes and surfacing anomalies for human review before they become regulatory findings. This monitoring function is not a post-hoc audit; it should be embedded in the production decisioning environment as an ongoing operational control.

How Fast Can an Automated Loan Decisioning System Make a Credit Decision?

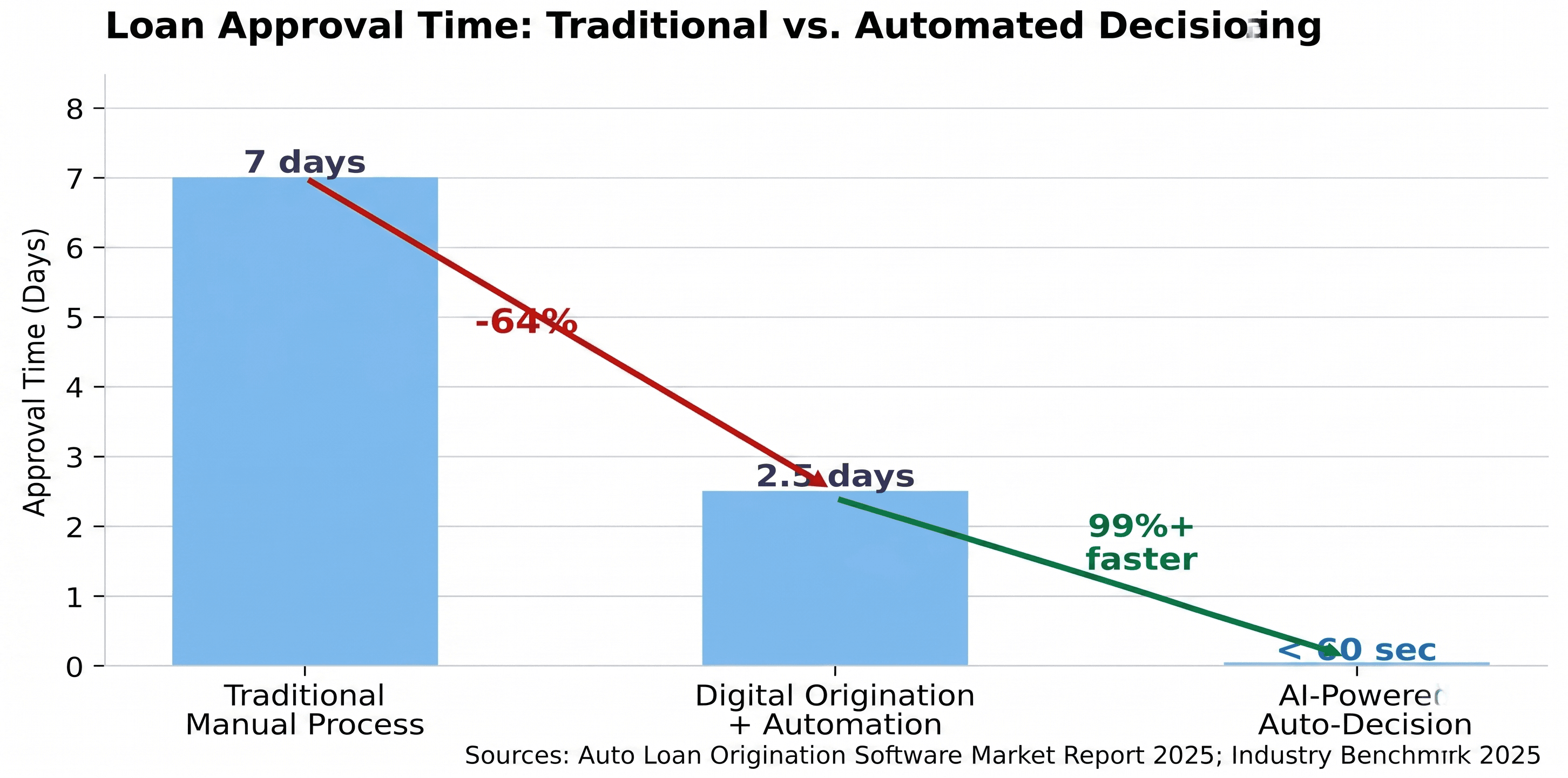

Speed in automated loan decisioning is not a single number it is a function of architecture, integration depth, and how the institution has configured its decisioning workflow. But the order of magnitude is clear: modern AI-powered decisioning systems return decisions in seconds, not hours or days.

The Four Enablers of Real-Time Decisioning

- Parallel data retrieval. Traditional decisioning required sequential data gathering: order a credit report, wait, then income verification, wait, then manual document review. Modern platforms query all data sources simultaneously at application submission, collapsing multi-step processes into a single parallel operation.

- Real-time AI inference. Machine learning models evaluate new applications in milliseconds once trained and deployed. What historically slowed decisioning was data gathering and human scheduling — not the evaluation itself.

- Pre-configured decisioning tiers. The fastest systems differentiate application types at intake and route them appropriately. Straightforward applications for existing members with deep account histories take a shorter path; new-member applications with limited credit history are routed to loan officers with all data pre-assembled.

- Direct core integration. Decision speed only translates to member-facing speed when connected to a core system that can act immediately. A decision engine returning an approval in 3 seconds but requiring manual data re-entry before booking eliminates most of the speed advantage.

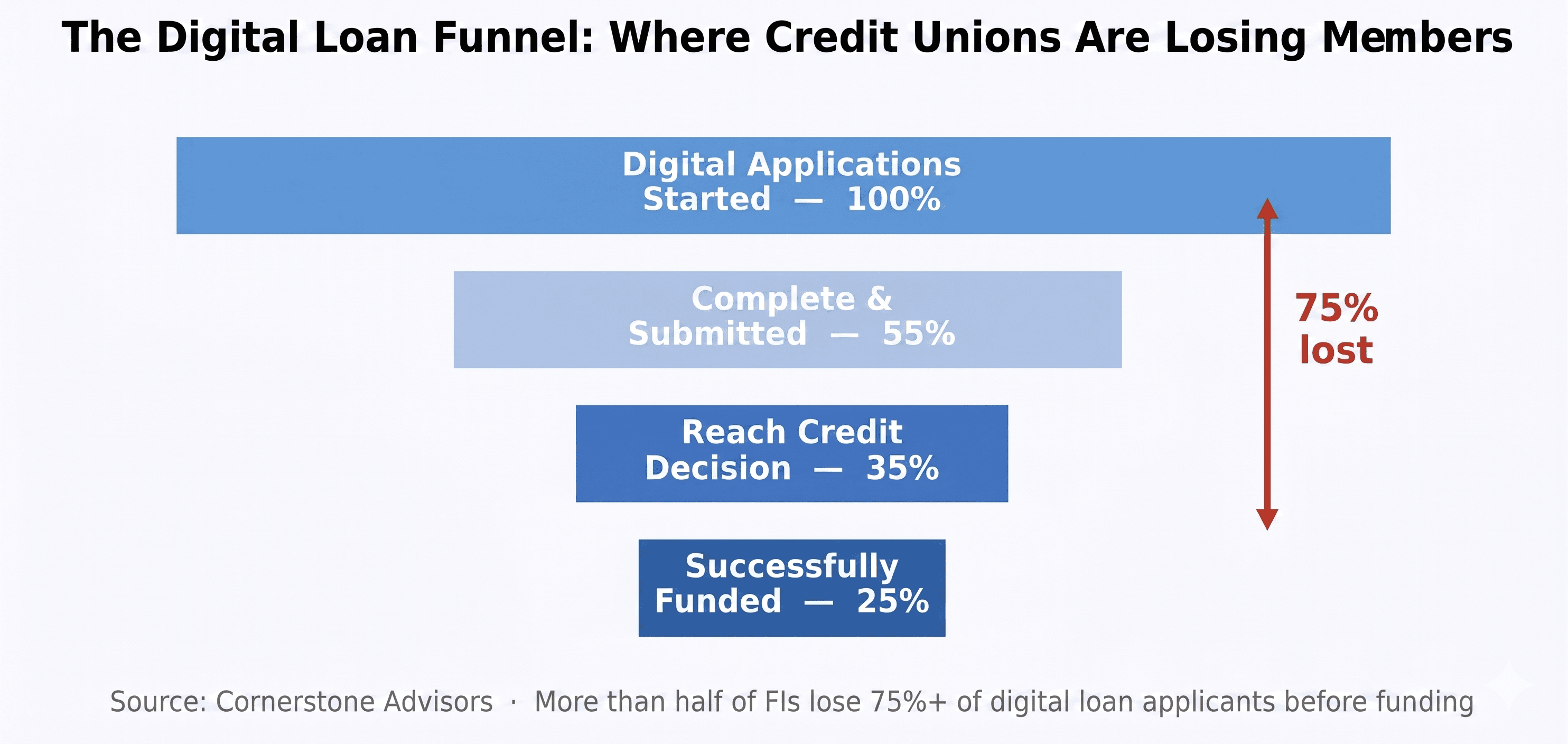

In practice, institutions operating modern AI-powered decisioning systems are consistently auto-decisioning 40 to 70 percent of consumer loan applications in under 60 seconds. Applications that require manual review are routed to underwriters with all data pre-assembled and a risk assessment already generated converting the underwriter's role from data gatherer to decision validator. The institutions that have deployed these systems report funding time reductions of one to two days compared to their previous workflows, with instant approval rates increasing by 25 percent or more.

Why Loan Decisioning Matters Differently for Credit Unions

The case for automated loan decisioning is compelling for any lender. For credit unions, the stakes are sharper in two specific directions and understanding both is essential for making the right investment.

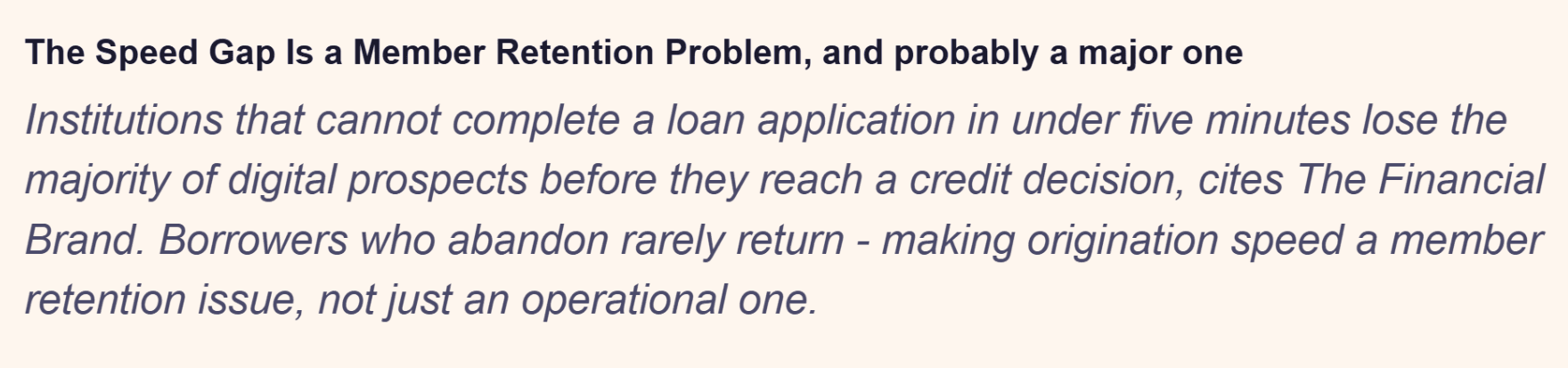

Competitive speed. Fintechs and major banks have established same-day or near-instant lending as the expected baseline for consumer loans. Credit union members particularly younger members are comparison-shopping on speed as much as rate and terms. A credit union whose lending decision process takes days is functionally inviting members to close a loan with a faster competitor while the application is in queue. Automated decisioning is not a technology upgrade for credit unions; it is a member retention strategy.

Inclusive lending as a mission obligation. Credit unions exist to serve members who may not have access to financial services elsewhere including members with thin credit files, non-traditional income, or credit histories that do not conform to the narrow parameters of classic scoring models. AI-powered decisioning systems that incorporate alternative data can approve members who a rules-based system would have denied, while maintaining or improving portfolio risk performance. AI-based scoring models have shown approval rate increases of 20 to 30 percent for previously unscorable borrowers without a corresponding increase in default rates. For a credit union, that is not just a business outcome it is the mission in operation.

The balance between these two objectives moving fast and lending inclusively is exactly where the design of the decisioning system matters most. Speed without accuracy produces bad loans. Accuracy without speed loses members. The right system delivers both.

The Algebrik AI Decisioning Engine: Built for Both Speed and Compliance

Algebrik One includes an AI-powered Decision Engine designed specifically for the credit union lending environment where speed, compliance, and inclusive member outcomes are not competing priorities but interconnected requirements.

Configurable policy rules with AI risk stratification. The Algebrik Decision Engine allows lending teams to configure hard policy floors and approval tiers directly - no developer required while AI models operate within those policy boundaries to evaluate the full risk profile of each application. Institutions retain full control of their underwriting standards while benefiting from AI's predictive accuracy within those standards.

Scienaptic AI integration for advanced decisioning signals. Through Algebrik's strategic partnership with Scienaptic AI, credit unions can access AI-powered credit decisioning signals including prescreen, fraud screen, application cross-sell, and renewal decisioning directly within the Algebrik LOS workflow. Scienaptic's platform processes over 3 million credit decisions per month and has helped more than 1.7 million underserved individuals access credit previously out of reach. Decision outcomes, conditions, and next-best-action recommendations surface directly in Algebrik's lender views, keeping loan officers in a single system of record.

Explainable outputs for ECOA compliance. Every decision generated by the Algebrik Decision Engine produces specific, human-readable reason codes mapped to the actual input factors that drove the outcome satisfying ECOA's specific-reasons requirement for adverse action notices without manual post-processing.

Real-time data integrations. Algebrik's integration with J.D. Power for auto loan valuation data ensures collateral values used in decisioning reflect real-time market conditions. Bureau integrations, income verification, and identity verification services are queried in parallel at application intake, not sequentially after manual data entry.

Same-day funding architecture. The Algebrik Decision Engine is connected directly to the full Algebrik One suite Digital Account Opening, Omnichannel POS, Lender's Cockpit, and core system integration so that a decision rendered in seconds can move immediately to document generation, e-signature, and core system funding without re-keying data or crossing system boundaries.

Frequently Asked Questions

What is loan decisioning software and how does it automate credit decisions?

Loan decisioning software is a technology platform that evaluates a borrower's creditworthiness and renders an approval, denial, or referral decision automatically without requiring manual underwriting for each application. It works by pulling data from credit bureaus, income verification services, fraud detection providers, and alternative data sources simultaneously, then applying configurable credit policy rules and/or machine learning models to generate a risk-based decision and the reason codes required for regulatory compliance. Automation comes from both parallel data retrieval and computational evaluation collapsing a process that once took days of sequential manual work into a decision that takes seconds.

What is the difference between a rules-based loan decision engine and an AI model?

How does automated loan decisioning ensure FCRA and ECOA compliance?

What data inputs does loan decisioning software use to approve or deny applications?

How fast can an automated loan decisioning system make a credit decision?

Ready to get started?

More Blogs

Blog

Computerized Loan Origination: How Technology Transformed Lending

Blog

Loan Origination System Requirements: A Checklist Before You Buy

Blog

Consumer Finance Systems: Why Unified Platforms Win Over Fragmented Stacks