‹ All Blogs

‹ All BlogsComputerized Loan Origination: How Technology Transformed Lending

Picture this: it is 1984. A borrower named William Bolt applies for a mortgage....

Lending Was Never Supposed to Take This Long

Picture this: it is 1984. A borrower named William Bolt applies for a mortgage. His banker, armed with one of the first-ever computerized loan origination systems, delivers an approval in two weeks. The Wall Street Journal calls it a revolution.

Fast-forward to today, and two weeks sounds almost quaint. Borrowers - especially the next generation of credit union members, expect decisions in minutes, funding in hours, and a digital experience that rivals anything their bank or fintech competitor offers.

The question for credit union decision-makers is not whether to modernize. It is whether your current loan origination system is keeping pace with what members now consider the bare minimum.

This article traces the full arc of computerized loan origination from its clunky 1980s roots to the cloud-native, AI-powered suites reshaping lending today and explains what that evolution means for your institution right now.

What Is a Computerized Loan Origination System?

A computerized loan origination system (LOS) is a software platform that manages the complete lifecycle of a loan - from the moment a member submits an application through underwriting, approval, documentation, compliance, and final funding. Rather than relying on manual handoffs, paper files, and siloed spreadsheets, a computerized LOS centralizes every step into a digital workflow.

At its core, a loan origination system handles:

- Application intake - capturing borrower data through digital forms, mobile apps, or branch channels

- Document collection and verification - validating income, identity, and collateral documents

- Credit decisioning - evaluating risk through bureau data, scoring models, and underwriting rules

- Compliance management - ensuring disclosures, calculations, and audit trails meet regulatory requirements

- Funding and closing - coordinating e-signatures, disbursements, and core system updates

For decades, these functions existed in disconnected silos. The transformation of lending has been, at its heart, the story of connecting those silos — and then replacing them entirely.

A Brief History: From Paper Stacks to AI Pipelines

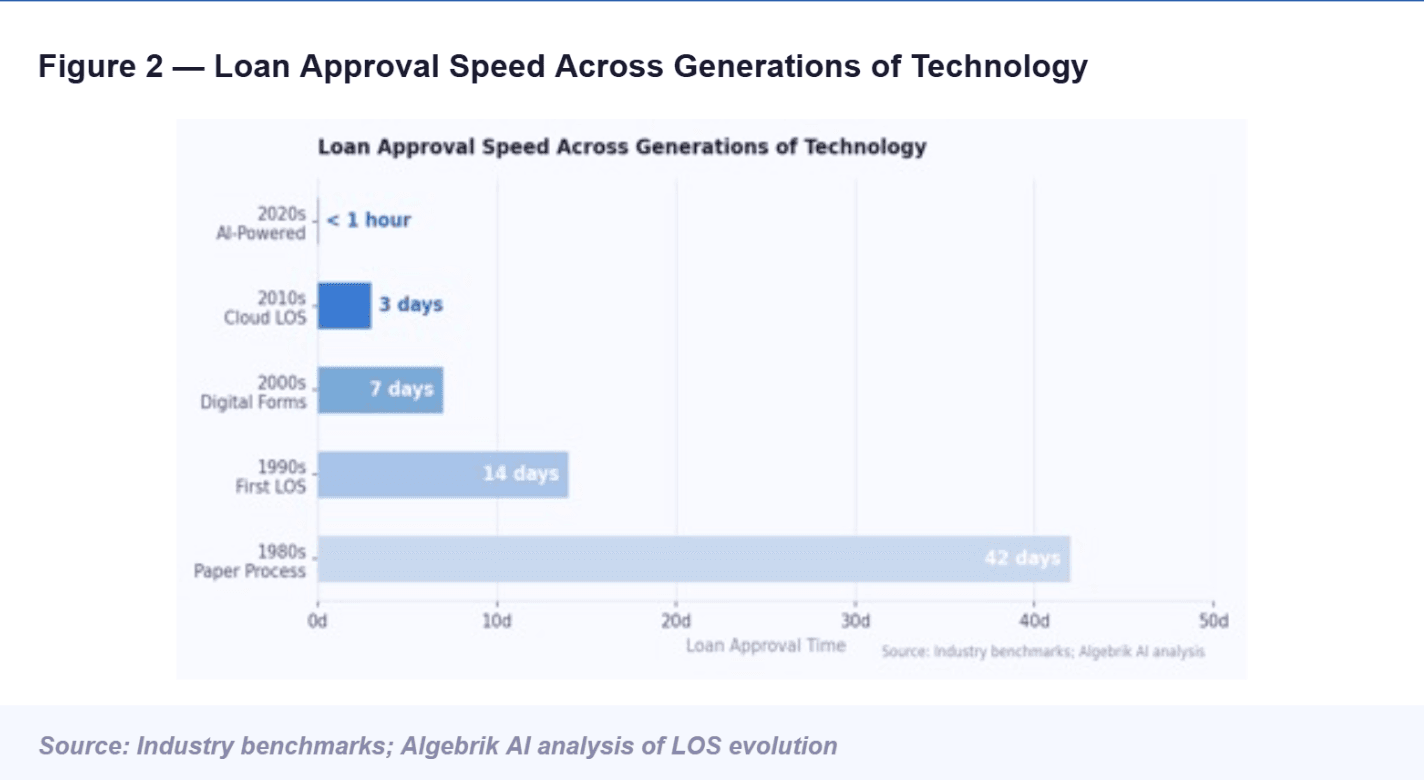

The earliest computerized loan origination systems emerged in the early-to-mid 1980s. They were single-lender tools - limited, slow by modern standards, but genuinely transformative at the time. Cutting a mortgage approval from six weeks to two weeks was considered extraordinary. What those early systems could not do was talk to each other. Point-of-sale systems, underwriting tools, and core banking platforms each lived in their own silo. Every loan still required stacks of paper, multiple handoffs, telephone calls, and faxes.

The internet era brought online application portals and the first generation of integrated LOS platforms. Lenders could accept digital applications, automate basic credit pulls, and begin connecting their origination workflows to core banking systems. Progress was real, but integration remained complex and expensive. Legacy architecture limited what was possible, and most systems were built for a world of in-branch, manual-review lending.

Cloud computing changed the economics of LOS deployment. Institutions no longer needed to host expensive on-premises servers. Software could be updated continuously rather than in annual release cycles. Mobile-first borrowers arrived expecting the same frictionless experience they got from streaming services and ride-sharing apps - but most lending platforms had not caught up.

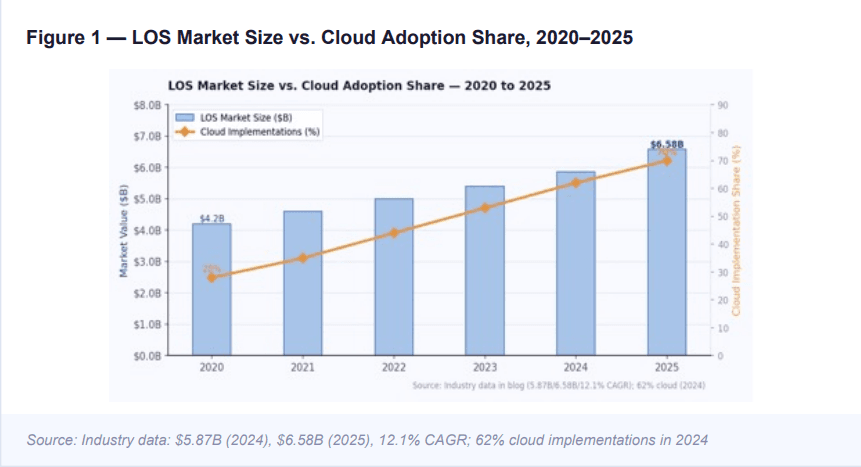

The current decade marks the sharpest inflection point in lending technology history. According to industry data, the global loan origination software market stood at $5.87 billion in 2024 and is projected to reach $6.58 billion in 2025 - growing at a 12.1% compound annual rate. Approximately 62% of new LOS implementations in 2024 were cloud-based, signaling a decisive industry shift away from on-premises infrastructure.

More significant than the market size is the nature of what is being built. AI-native origination platforms are not simply faster versions of older systems - they represent a fundamentally different architecture where intelligence is embedded at every decision point, not bolted on as an afterthought.

How Has Technology Changed the Loan Origination Process Over the Last Decade?

The last ten years have compressed more change into lending technology than the previous thirty combined. Here are the five most consequential shifts:

Traditional LOS platforms moved loan applications through discrete, sequential stages - intake, then underwriting, then compliance, then closing with handoffs and waiting periods between each. Modern systems replace this with continuous, parallel workflows where multiple processes run simultaneously. A borrower's identity can be verified while their income is being analyzed and their compliance disclosures are being auto-generated.

A decade ago, most credit union loans originated at the branch. Today, members expect to start an application on their phone, receive a decision via text, and complete e-signing from their laptop - without repeating a single step. Omnichannel origination requires a platform architecture that treats every channel as a first-class experience, not a bolt-on portal.

Legacy underwriting relied on fixed rule sets - credit score thresholds, DTI limits, LTV ratios - applied uniformly regardless of context. Modern AI-powered decisioning evaluates hundreds of data points dynamically, incorporating trended bureau data, alternative credit signals, and behavioral indicators. The result is more accurate risk assessment and more inclusive outcomes for members with thin or non-traditional credit files.

Document management was one of the most labor-intensive aspects of traditional lending. AI-powered optical character recognition (OCR) and document intelligence now automatically extract, validate, and organize data from pay stubs, tax returns, and bank statements - eliminating the back-and-forth between loan officers and members that historically added days to origination timelines.

Perhaps the most visible change is speed. Fintechs and major banks have conditioned borrowers to expect near-instant decisions. Credit unions that cannot match this pace face a real competitive disadvantage not because members do not value the relationship, but because the friction of waiting too long will send them elsewhere before the relationship can be preserved.

What Is the Role of AI in Modern Computerized Loan Origination Systems?

AI is not a feature in a modern LOS - it is the foundation. The distinction matters because it determines what a platform can actually do, not just what it can claim.

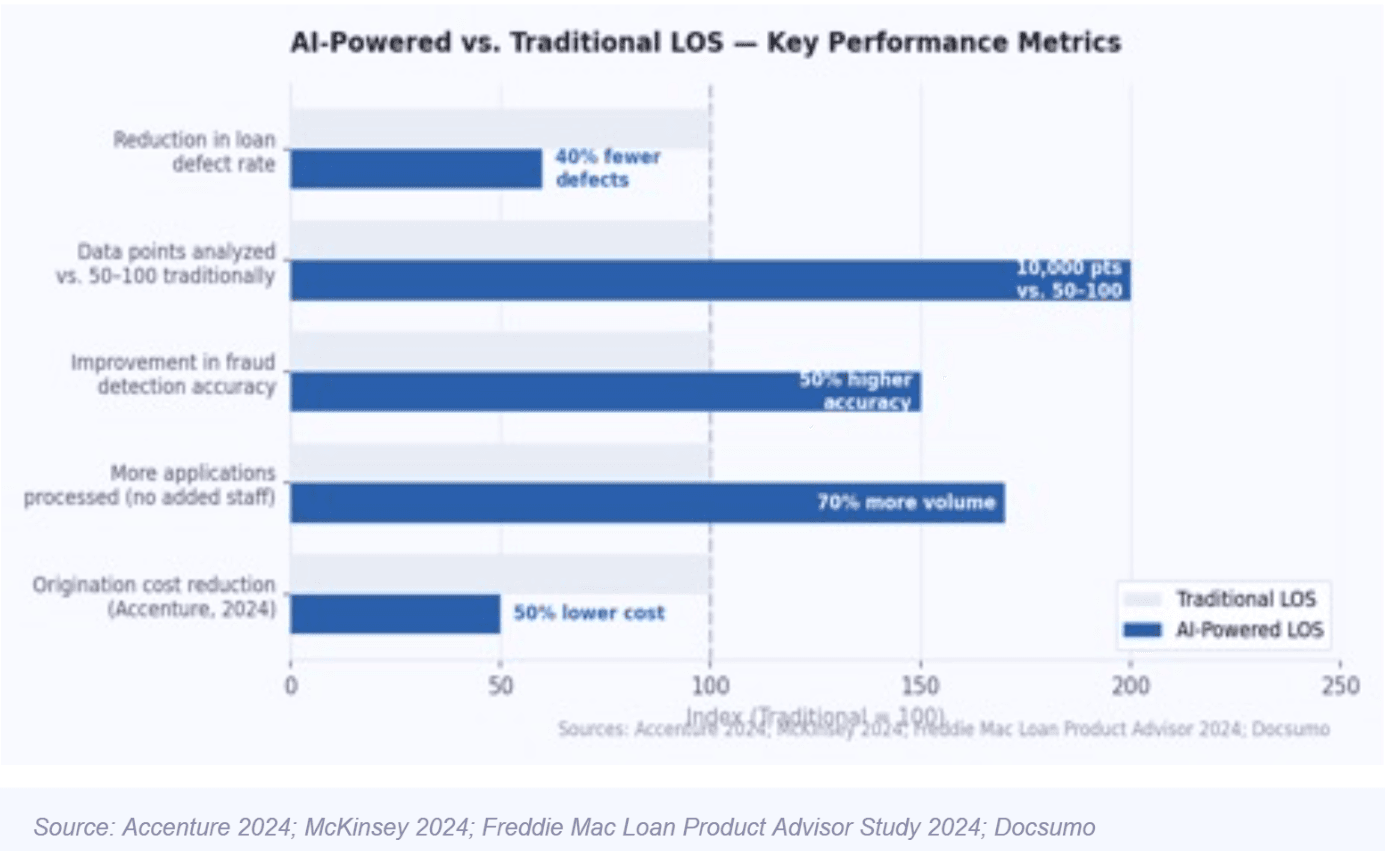

Traditional credit scoring uses a handful of variables evaluated at a single point in time. AI-powered decisioning analyzes far richer datasets - including trended credit behavior, income volatility, alternative data sources, and macroeconomic signals - and updates those evaluations continuously. Credit unions using AI-assisted underwriting have reported processing up to 70% more loan applications without adding underwriting staff. Early adopters of generative AI underwriting tools are reporting efficiency gains of three to five times compared to manual workflows.

AI document intelligence goes beyond scanning. It reads, interprets, and cross-validates information across multiple documents simultaneously - flagging discrepancies, identifying potential fraud, and surfacing exceptions for human review rather than routing every file through a manual queue. This approach dramatically shortens cycle times while improving accuracy.

AI enables credit unions to move from reactive to proactive lending. Rather than waiting for a member to submit an application, AI systems analyze spending patterns, income trajectories, and lifecycle events to surface pre-approved offers at the right moment - before the member goes elsewhere. This is not just efficiency; it is a meaningful enhancement of the member relationship.

AI models continuously monitor application data and behavioral signals for fraud indicators. Because these models update in real time rather than relying on static rule sets, they adapt to emerging fraud patterns faster than any manual process can.

The Difference Between a Computerized LOS and an AI-Powered LOS

A computerized LOS automates manual tasks - it digitizes the existing process. An AI-powered LOS transforms the process itself. Where a traditional LOS applies your underwriting rules consistently, an AI-powered system learns, adapts, and improves decision accuracy over time. Where a legacy system requires IT intervention to adjust workflows, an AI-native platform allows lenders to configure and modify processes directly. The operational ceiling of a computerized LOS is a faster version of what your team already does. The ceiling of an AI-powered LOS is a lending operation that becomes more intelligent with every application it processes.

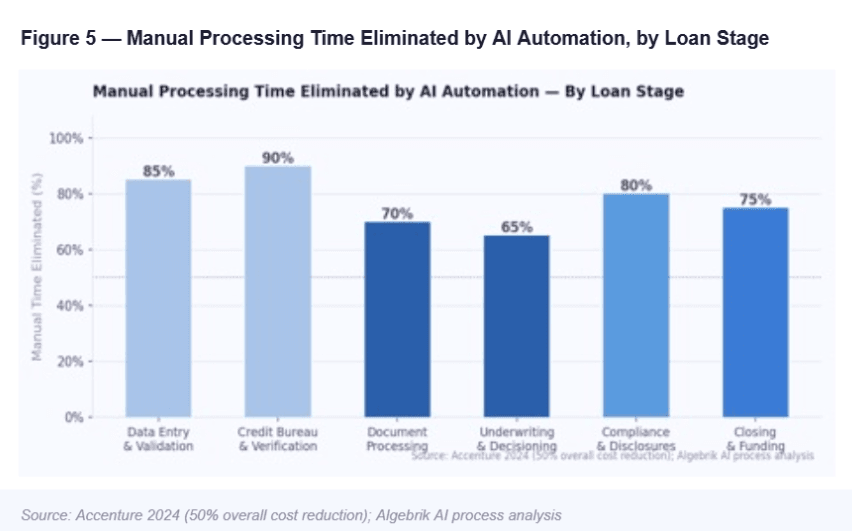

How Does Automated Loan Origination Reduce Manual Processing Time?

The time reduction from automated loan origination is not incremental - it is structural. Here is where the biggest gains come from:

Instant data capture and validation. Digital application forms pre-populate fields from verified data sources, validate inputs in real time, and flag incomplete or inconsistent information before the application is even submitted. The error rate in manual data entry disappears.

Automated bureau and verification pulls. Rather than a loan officer manually ordering credit reports, income verification, and identity checks - and waiting for each to return - automated origination platforms trigger all of these simultaneously the moment an application is submitted.

Rules-based auto-decisioning. For applications that fall clearly within policy, AI decision engines render approvals, counters, or declines in seconds. Human underwriters are routed only the cases that genuinely require judgment - complex income situations, exceptions, or high-value relationships - rather than every application in the queue.

Automated compliance and disclosure generation. Compliance calculations are embedded directly in the origination workflow. Disclosures generate automatically based on loan type, jurisdiction, and product parameters, drawing on the correct calculation methodology without manual intervention.

Integrated e-signatures and core updates. Electronic document execution eliminates the scheduling delays of in-person signing, and direct core system integration means funding can be triggered the moment documents are complete — without re-keying data into a separate system.

The cumulative effect of eliminating each of these bottlenecks is profound. Institutions that have implemented AI-driven automation in their origination workflows have reported processing cost reductions of 30 to 40 percent per loan, with corresponding improvements in member satisfaction scores driven by faster, more transparent experiences.

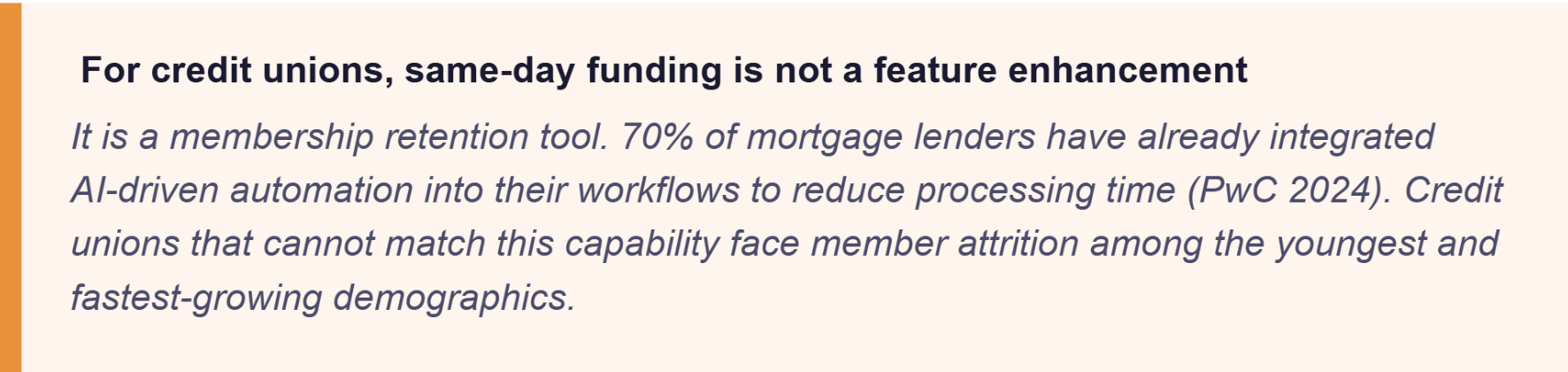

How Do Modern Loan Origination Systems Enable Same-Day Funding?

Same-day funding, once the exclusive territory of fintech lenders is now achievable for credit unions with the right platform architecture. Three capabilities make it possible:

Same-day funding requires that credit decisions happen in minutes, not hours. AI-powered decision engines evaluate applications against policy parameters, bureau data, and risk models instantly - without queuing for a human underwriter's review in straightforward cases. When the decision environment is configured correctly, approvals for qualified members can be rendered before they have closed their browser tab.

No single system contains all the data needed to fund a loan. Same-day origination requires real-time integrations with credit bureaus, income verification services, fraud detection platforms, compliance calculation engines, and core banking systems - all operating within a unified workflow rather than requiring manual data transfer between separate tools. Modern API-first LOS platforms make these integrations configurable without custom engineering work.

E-signature integrations eliminate the document turnaround lag that historically delayed funding. Once documents are executed, a modern LOS pushes the completed loan directly to the core system and triggers disbursement - often within the same business day the application was submitted.

For credit unions competing against fintechs and regional banks on speed, this capability is not a feature enhancement. It is a membership retention tool.

What Credit Unions Need in a Modern LOS and What Most Platforms Still Miss

Despite the advances in lending technology, the reality for many credit unions is that their current LOS was built for a different era. Legacy platforms - even those with modern interfaces layered on top, were designed around sequential workflows, manual review queues, and single-channel member interactions.

The gaps most credit unions still encounter include:

Broken omnichannel journeys: A member who starts an application on mobile and continues at a branch should not have to start over. Most legacy systems cannot preserve context across channels - creating exactly the kind of friction that drives members to competitors.

High abandonment rates: Industry research consistently shows that application abandonment is a primary driver of lost loan volume. Complex, slow, or confusing digital application experiences - often the result of platforms designed for loan officers rather than borrowers - are a significant cause.

IT dependency for workflow changes: Credit union lending strategies change in response to member needs, competitive pressures, and macroeconomic conditions. A platform that requires IT tickets to adjust underwriting rules, product parameters, or communication workflows cannot keep pace with a market that moves in real time.

Fragmented vendor relationships: Managing separate vendors for POS, LOS, document management, e-signatures, and analytics creates integration complexity, support fragmentation, and data reconciliation problems that consume operational resources without adding member value.

Algebrik One: Built for the Modern Lending Reality

Algebrik AI exists precisely because the lending technology industry has not kept pace with the needs of credit unions and their members. In an industry that had not seen meaningful innovation in lending platforms for more than 25 years, Algebrik One was built from scratch - cloud-native, AI-powered, and designed for the next generation of members from day one.

Algebrik One is not a digitized version of legacy lending. It is a unified, end-to-end loan origination suite that turns disconnected lending steps into one continuous, automated origination process.

Digital Account Opening: enables members to open accounts and apply for loans through a fully digital experience - mobile, web, or branch - with a consistent, personalized journey across every channel.

Omnichannel Point of Sale: captures loan applications wherever the member is, preserving context and progress across channels so no member ever has to start over.

Lender's Cockpit: gives lending teams a single, centralized command center for managing applications, reviewing exceptions, communicating with members, and tracking pipeline performance - without switching between systems.

AI Decision Engine: evaluates applications against configurable policy parameters, bureau integrations, and risk models - rendering decisions in real time and routing complex cases for human review. Algebrik's partnership with Scienaptic AI brings advanced AI credit decisioning signals directly into the origination workflow, enabling more inclusive and accurate lending outcomes.

Portfolio Analytics: provides real-time visibility into origination performance, approval rates, cycle times, and portfolio risk - giving credit union leadership the data to make faster, more confident strategic decisions.

Compliance-Ready by Design: through integrations with Carleton for payment calculation and compliance APIs, Algebrik ensures accurate disclosures across 1,000+ calculation methods, including credit insurance, disability, and GAP coverage, adapting to lender-specific rules without manual intervention.

Core Integration: Algebrik's participation in the Jack Henry Vendor Integration Program and its integration with Corelation's KeyStone core system means that credit unions can connect Algebrik One to their existing infrastructure without bespoke IT builds.

The result is a lending operation where the technology handles the complexity and lending teams stay focused on members.

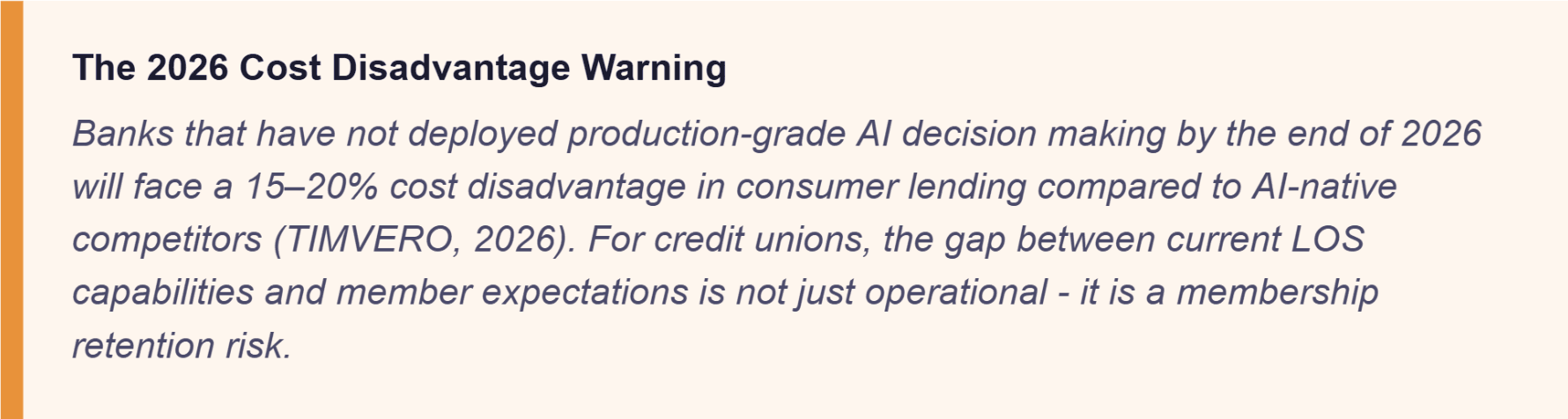

The Stakes for Credit Unions in 2026 and Beyond

The competitive landscape for credit union lending has fundamentally shifted. Fintechs and megabanks have already established same-day decisioning and digital-first experiences as the baseline expectation. For credit unions still operating on legacy LOS platforms, the gap is not just operational - it is existential for member retention among younger demographics.

Critically, AI in lending is no longer a competitive advantage. It is rapidly becoming the competitive baseline. Institutions that have not deployed production-grade AI in their origination workflows will face an increasingly difficult cost and speed disadvantage compared to AI-native competitors.

Credit unions have always held a structural advantage in member relationships, community trust, and alignment of interests. The question is whether the technology supporting lending is strong enough to deliver on those advantages in a digital-first world — or whether it is eroding them one abandoned application at a time.

Modernizing the loan origination system is not a technology upgrade. It is a member retention strategy.

Frequently Asked Questions

How has technology changed the loan origination process over the last decade ?

Over the last decade, loan origination has shifted from sequential, paper-heavy workflows to continuous, AI-automated processes. The most significant changes include omnichannel delivery, real-time AI decisioning, intelligent document processing, automated compliance generation, and same-day funding capabilities - all driven by cloud-native platform architectures that replace the siloed legacy systems of the previous generation.

What is the role of AI in modern computerized loan origination systems ?

How does automated loan origination reduce manual processing time ?

What is the difference between a computerized LOS and an AI-powered LOS ?

How do modern loan origination systems enable same-day funding ?

Ready to get started?

More Blogs

Blog

Loan Origination System Requirements: A Checklist Before You Buy

Blog

Consumer Finance Systems: Why Unified Platforms Win Over Fragmented Stacks

Blog

What are Loan Decisioning Softwares and Why Do they Matter?