‹ All Blogs

‹ All BlogsLoan Origination System Requirements: A Checklist Before You Buy

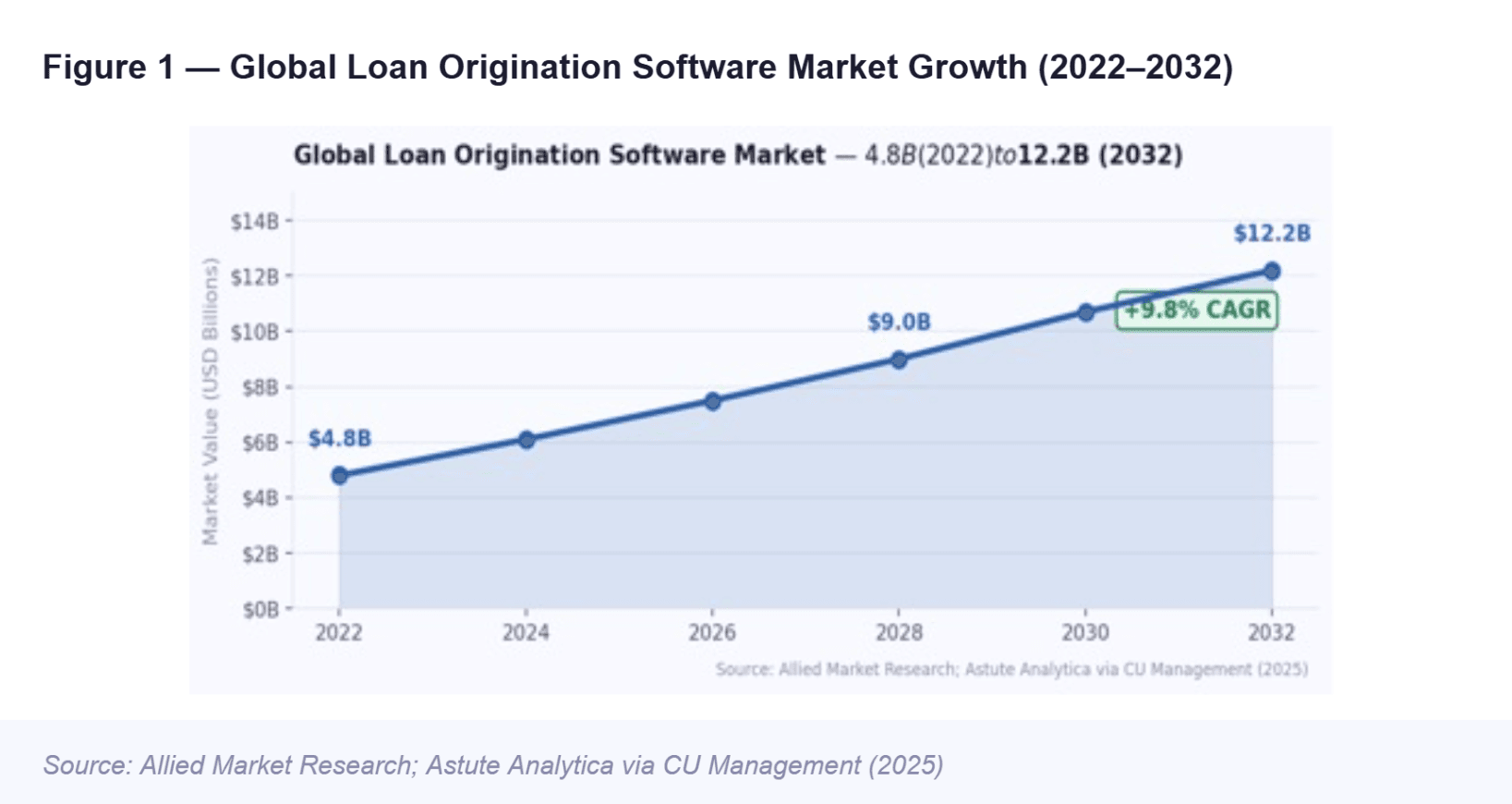

Selecting a loan origination system is one of the highest-stakes technology deci...

The Wrong LOS Is Expensive in Ways That Don't Show Up in the Contract

Selecting a loan origination system is one of the highest-stakes technology decisions a credit union leadership team will make. Get it right and your institution gains a platform that accelerates loan volume, deepens member relationships, and scales with your growth. Get it wrong and you inherit years of integration headaches, compliance exposure, abandoned applications, and a vendor relationship that costs more to exit than to endure.

The challenge is that most LOS evaluations happen under time pressure - a contract renewal deadline, a regulatory flag on the current system, or a competitor announcement that forces the conversation. Evaluation teams get vendor demos before they have aligned on what they actually need, and checklists get built in reverse: features first, requirements second.

This guide is designed to reverse that order. Before you issue an RFP, sit through a demo, or sign a pilot agreement, your team should align on the requirements that are non-negotiable - and the questions that will separate platforms built for the modern lending environment from those wearing a modern interface over outdated architecture.

What follows is a structured, role-tested checklist organized across six requirement domains that every credit union LOS evaluation should cover.

Why LOS Requirements Differ for Credit Unions

Before diving into the checklist, it is worth being precise about why credit union requirements differ from those of commercial banks or mortgage lenders - because the difference shapes everything downstream.

Credit unions are member-owned cooperatives governed by NCUA regulations, and they operate under a relationship-first mandate that commercial lenders are not obligated to honor. This creates specific requirements that generic LOS platforms often underweight:

Member experience is an obligation, not a marketing differentiator. When a credit union member has a poor digital lending experience, it is not just a lost loan - it is a breach of the cooperative relationship. LOS platforms that prioritize lender efficiency over borrower experience are a structural mismatch.

Compliance exposure runs directly to leadership. Credit unions under $10 billion in assets are supervised by the NCUA for ECOA compliance. Adverse action notice errors, one of the most common regulatory findings, are LOS process failures as much as they are training failures. The system your credit union uses determines how easy or hard it is to stay compliant.

Integration complexity is a real operational risk. Most credit unions run a single core processing system (Symitar, KeyStone, etc.) and cannot absorb the integration overhead that large banks can. An LOS that requires bespoke IT work to connect to your core is a perpetual resource drain.

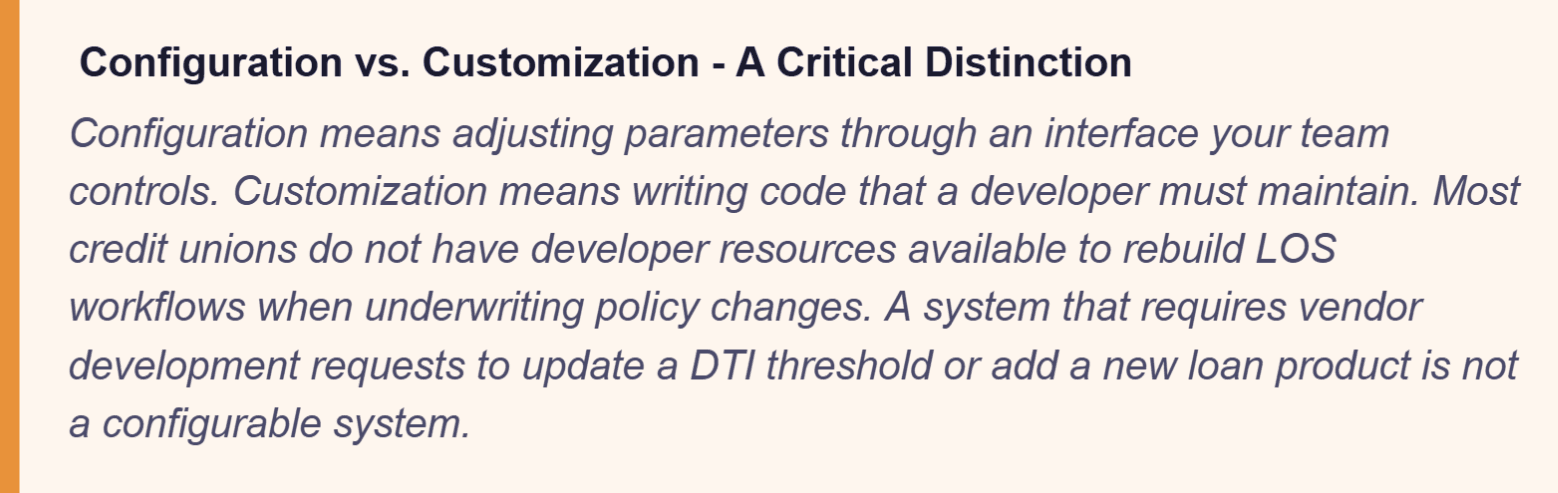

Configurable, not just customizable. The distinction between configuration- adjusting parameters through an interface; and customization: writing code, is critical for credit union operations teams. Most credit unions do not have developer resources available to rebuild LOS workflows when underwriting policy changes.

With that context, here is the checklist.

The 6-Domain LOS Requirements Checklist

These are the baseline capabilities an LOS must deliver to be viable for a credit union - not differentiators, but table stakes.

Multi-product loan origination support: The system must handle every loan product in your portfolio - consumer loans, auto loans, personal loans, HELOCs, and credit cards - within a single platform. An LOS that covers some products natively and requires separate systems for others creates the exact data fragmentation you are trying to eliminate.

Digital application intake across all channels: Member applications must be capturable through web, mobile, in-branch, and call center channels with a consistent experience across all of them. Critically, the system must preserve application context across channel switches - a member who starts on mobile and continues at a branch should not have to start over.

Configurable underwriting workflow: Lending teams must be able to configure underwriting rules, approval criteria, product parameters, and workflow stages through an interface - not through IT tickets or vendor development requests. As your underwriting policies evolve in response to market conditions and risk appetite, the LOS must adapt at the same pace.

AI-powered decisioning engine: Rule-based decisioning alone is no longer sufficient. The platform must include an AI or machine learning decisioning engine capable of evaluating bureau data, alternative credit signals, and behavioral indicators in real time - and generating explainable decisions that satisfy ECOA's requirement for specific adverse action reasons.

Document management and e-signature: The system must collect, validate, and store loan documents digitally - including income verification, identity documents, and collateral documentation and support electronic signature for closing without requiring a separate vendor relationship.

Automated stipulation management: The LOS must be able to generate, track, and clear loan stipulations automatically, with member-facing communication to request outstanding items and internal task routing for staff follow-up.

Core system integration - native, not manual: Direct API-based integration with your core processing system (Symitar, KeyStone, or equivalent) is non-negotiable. Manual data re-entry between the LOS and core is not a workaround - it is a source of errors, delays, and audit findings. Ask vendors for their specific integration method, not just whether integration exists.

This is the domain where incomplete evaluation creates the most serious institutional risk. Compliance requirements for credit union LOS platforms are specific, examinable, and non-negotiable.

What are the compliance capabilities a loan origination system must support for ECOA and adverse action?

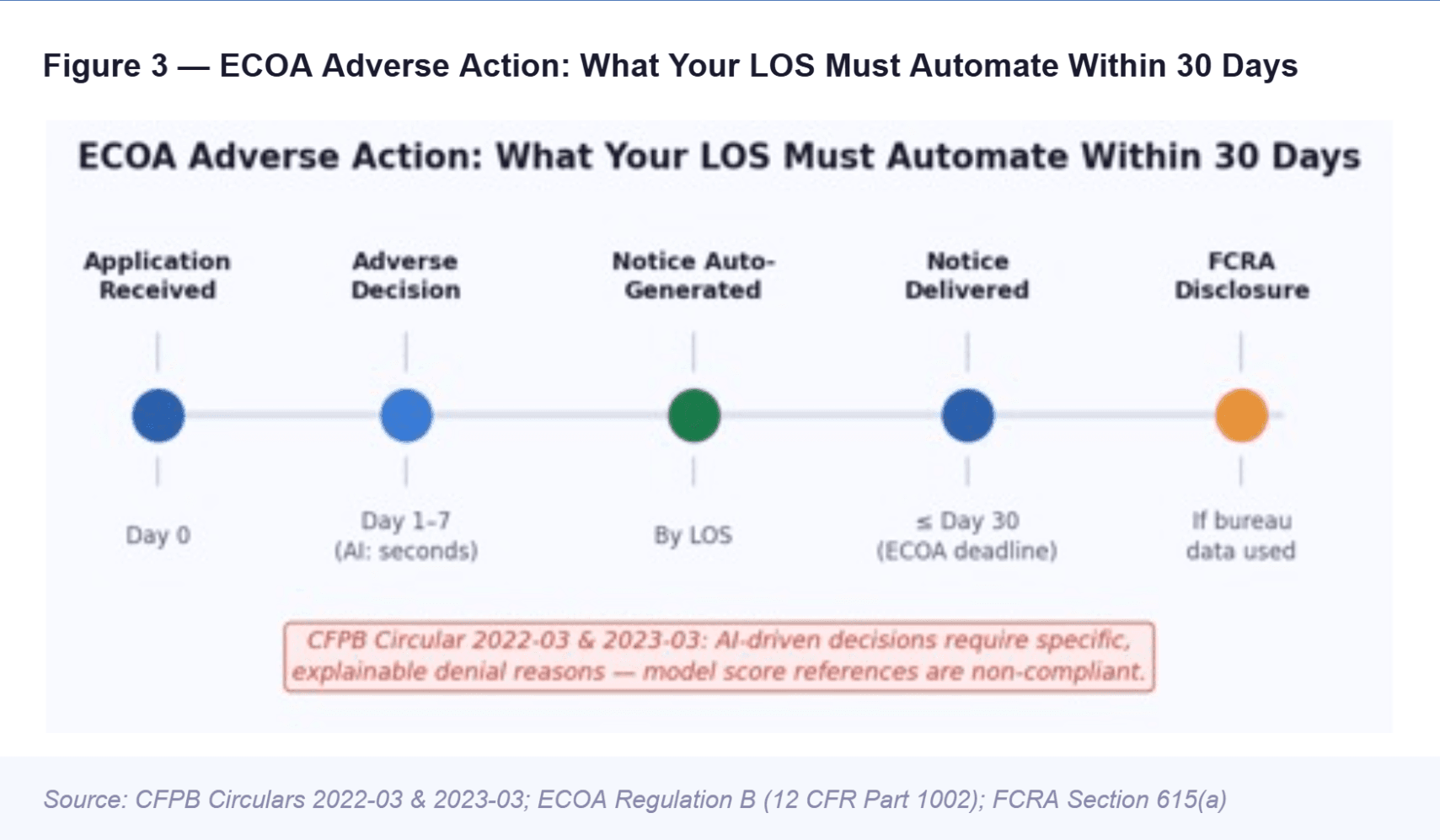

Under the Equal Credit Opportunity Act (ECOA) and its implementing Regulation B (12 CFR Part 1002), credit unions have specific, time-bound notification obligations whenever adverse action is taken on a completed credit application. Your LOS must support all of the following:

Automated adverse action notice generation: When a loan application is denied, the system must automatically generate a written adverse action notice within 30 days of receiving a completed application. Notices must include: the specific reasons for the adverse action (not general statements about internal policies), the creditor's name and address, an ECOA statement, and - when a credit report was used - the name and contact information of the consumer reporting agency.

Critical compliance note: The CFPB has explicitly clarified in Circular 2022-03 and 2023-03 that ECOA adverse action requirements apply equally to AI-driven decisions. An LOS that uses AI decisioning must be able to produce specific, human-readable reasons for each denial, not a model score or a reference to an algorithm. Evaluate this capability by asking vendors to show you a sample adverse action notice produced by their AI engine. Vague outputs are a compliance liability.

FCRA compliance for credit report disclosures: When adverse action is based in whole or in part on information from a consumer reporting agency, the system must also generate the required FCRA Section 615(a) disclosure including the CRA's name, address, and phone number, plus credit score information and the four factors most adversely impacting the score.

Application completeness tracking and incomplete application notices: If an application cannot be processed because of missing information, the LOS must generate written notice to the applicant specifying what is needed and setting a reasonable deadline. This notice must go out within 30 days of receiving the incomplete application.

Fair lending monitoring and HMDA reporting: The system must support fair lending analysis enabling your compliance team to monitor approval and denial rates across protected classes and generate HMDA-required data fields where applicable to your loan products.

BSA/AML and KYC identity verification: The LOS must integrate with identity verification and watchlist screening services to satisfy Bank Secrecy Act and Customer Due Diligence requirements at application intake. Embedded verification rather than a manual step outside the system, is essential for cycle time and audit trail integrity.

Calculation accuracy and disclosure compliance: For payment calculations, APR disclosures, and Truth in Lending Act (TILA) requirements, the system must use verified, auditable calculation methodologies. Verify that the vendor can demonstrate compliance across all loan product types in your portfolio, including credit insurance and GAP products if applicable.

Regulatory change management: Compliance requirements change. Ask every vendor: how do regulatory updates get reflected in the platform? Who is responsible your team or the vendor? How long does it take? A platform that leaves regulatory updates to client-side configuration is a different risk profile than one where updates are pushed by the vendor.

What security certifications should a loan origination system have?

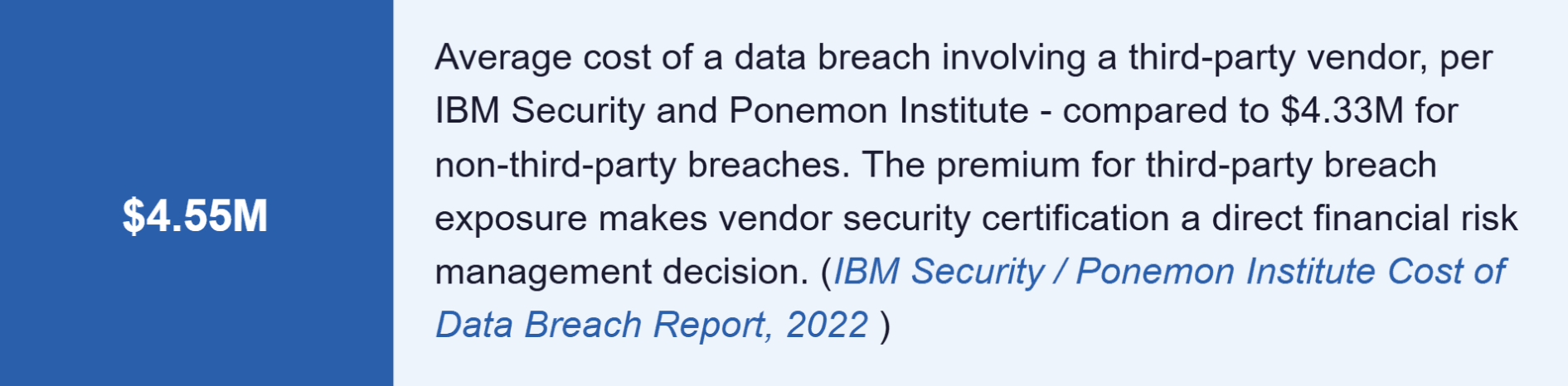

An LOS handles some of the most sensitive financial and personal data your institution manages - income records, identity documents, credit history, Social Security numbers. Security certification is not a vendor marketing point; it is an examiner expectation and a member trust obligation.

SOC 2 Type II certification - required, not preferred SOC 2 Type II is the standard security attestation for cloud-based financial services platforms. Unlike SOC 2 Type I (which evaluates controls at a single point in time), SOC 2 Type II evaluates whether security controls functioned effectively over a sustained period - typically 3 to 12 months. This distinction matters because Type I reports tell you the controls were designed correctly; Type II reports tell you the controls actually worked.

Specifically, a credit union LOS should hold SOC 2 Type II attestation covering at minimum the Security Trust Services Criterion (which is always required) and ideally Availability and Confidentiality criteria as well. Do not accept a SOC 2 Type I report as a substitute for a vendor that has been operating for more than a year.

ISO 27001 alignment or certification ISO 27001 is the international standard for information security management systems. While not universally required, vendors who hold or align to ISO 27001 demonstrate a systematic approach to information security governance rather than point-in-time control testing.

Encryption standards All data must be encrypted in transit (TLS 1.2 or higher) and at rest (AES-256 or equivalent). Ask vendors to confirm encryption standards explicitly — and to confirm that encryption applies to data stored in third-party integrations as well as within their own infrastructure.

Role-based access controls and audit logging The system must enforce role-based access so that staff can only view and act on loan data appropriate to their function. Every access event, data modification, and decision must be logged with timestamps and user attribution — creating the audit trail your compliance team needs and your examiners will look for.

Penetration testing and vulnerability disclosure Ask vendors when their last third-party penetration test was conducted, what findings were identified, and how remediation was handled. A vendor that cannot or will not share this information is a vendor that has not made security a priority.

Vendor subprocessor transparency Cloud-native LOS platforms typically rely on subprocessors - cloud infrastructure providers, identity verification services, bureau integrations - that also handle your member data. Ask for a complete subprocessor list and confirm that each subprocessor holds equivalent security standards.

API-first architecture Modern LOS platforms are built around open, documented APIs that allow your institution to connect to bureau services, verification providers, core systems, and third-party fintech tools without custom development work. Proprietary integration architectures - where the vendor controls every connection - create vendor lock-in and limit your ability to adopt better-fit solutions for specific functions.

Core banking system integration - named and certified Ask the vendor to name the specific cores they integrate with and to describe the integration method. Participation in vendor integration programs (like Jack Henry's VIP program) provides a meaningful signal of integration depth and support. Corelation's KeyStone, Symitar, and other major credit union cores should be on the certified integration list if they are relevant to your institution.

Bureau and third-party data integrations The LOS must support direct integrations with the credit bureaus your institution uses for credit pulls, as well as income verification, fraud detection, and identity verification services. Evaluate whether these integrations are native (built and maintained by the LOS vendor) or rely on the credit union to build and maintain them independently.

Cloud-native deployment On-premises LOS deployments are architecturally incompatible with the integration density, update frequency, and scalability that modern lending operations require. Confirm that the platform is built and deployed as a cloud-native application - not a legacy platform hosted in the cloud, which is a meaningfully different thing.

Composable workflow architecture The platform should support composable or microservices-based workflow design - meaning individual workflow components can be updated, replaced, or extended independently without affecting the entire system. This architectural property is what allows credit unions to adapt their origination workflows in response to market conditions without waiting for a vendor release cycle.

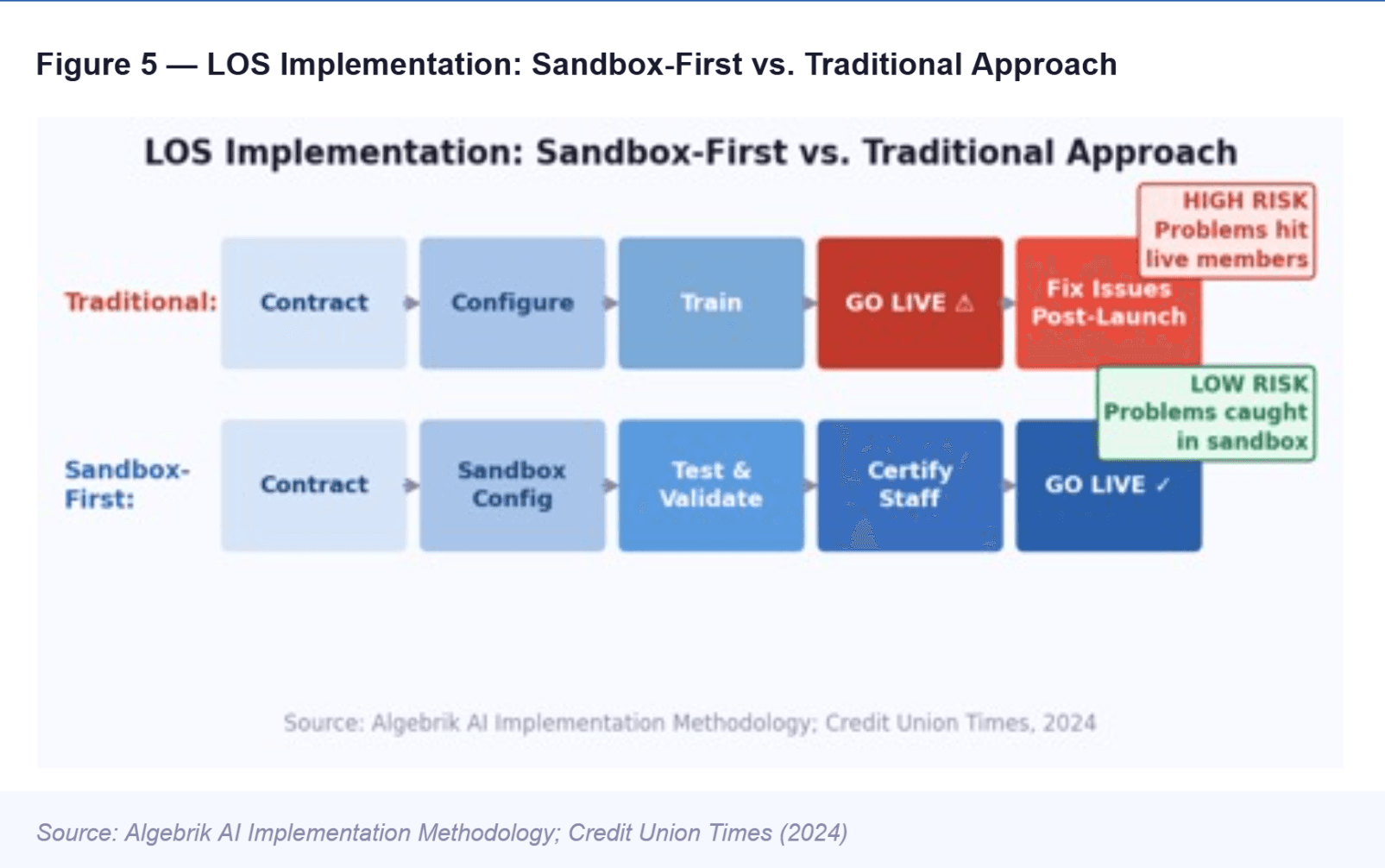

What is a sandbox-first LOS implementation and why is it better?

Implementation is where LOS evaluations most commonly underestimate risk. A system that works in a demo environment may behave very differently when connected to your core, loaded with your product configurations, and operated by your team under real lending conditions.

A sandbox-first implementation approach means the vendor provisions a fully functional, isolated environment that mirrors your production configuration before any live data or real member interactions are involved. Your team configures, tests, and validates workflows in the sandbox until all integrations, products, and decisioning rules are confirmed to work as expected - and only then does the system go live.

Why sandbox-first is better: It eliminates the risk of discovering integration problems after launch, when they affect real members and live loans. It gives your operations and compliance teams the time to validate adverse action outputs, verify calculation accuracy, and test edge cases - including the unusual loan scenarios that demos never cover. It also creates a training environment that persists after launch, allowing new staff to practice in a realistic system without touching production data.

Dedicated implementation project management Require a named implementation project manager– not a shared support queue - who is accountable for your go-live timeline, issue escalation, and configuration validation. Implementation failures are almost always the result of diffuse accountability, not technical complexity.

Data migration plan and validation If you are replacing an existing LOS, the vendor must provide a documented data migration methodology - including how in-flight loans, historical data, and member records will be transferred, validated, and reconciled. Request evidence of prior migrations from your existing platform to theirs.

Staff training and role-based certification The vendor should provide structured training aligned to each staff role - loan officers, underwriters, compliance, operations -not a single generic user guide. Training should be available both during implementation and on-demand post-launch for new hire onboarding.

Parallel run period Before fully decommissioning your previous system, require a defined parallel run period during which both systems process loans simultaneously. This validates that the new LOS is performing as expected before the institution is fully dependent on it.

What SLA and support standards should you require from an LOS vendor?

The service level agreement is where vendor commitments become contractual. Most vendors offer standard SLAs as a starting point - the NCUA's vendor management guidance explicitly recognizes that these are negotiable. Credit unions should treat the standard SLA as a floor, not a ceiling.

99.9% or higher uptime guarantee - with penalties: A 99.9% uptime guarantee allows for approximately 8.7 hours of downtime per year. For a lending platform where same-day funding is a competitive requirement, even that threshold may be insufficient during peak hours. The SLA must define: how uptime is calculated (excluding or including planned maintenance), what counts as a system outage versus degraded performance, and what financial penalties or service credits apply when uptime targets are missed.

Do not accept an SLA without teeth. Uptime guarantees that carry no financial consequence are aspirational statements, not contractual commitments.

Defined response and resolution time tiers: The SLA must specify response and resolution timeframes for incidents by severity level typically P1 (system-down), P2 (major functionality impaired), and P3 (minor issues). P1 incidents that prevent loan origination should require response within 30 minutes and resolution acknowledgment within 2 hours. Ask the vendor for their actual P1 response time data from the previous 12 months.

Dedicated named support contact post-implementation: Ticket queues and rotating support agents are not acceptable for an institution's primary lending platform. Require a dedicated customer success manager or account team with knowledge of your specific configuration, core integration, and compliance setup.

Regulatory update SLA: When a compliance requirement changes a CFPB circular, a Regulation B amendment, a new NCUA supervisory priority your LOS must be updated to reflect the new requirement. The vendor SLA should specify how regulatory changes are communicated, what the implementation timeline is, and who is responsible for configuration updates. Leaving regulatory compliance updates to your internal team is an institutional risk, not a cost-saving measure.

Data portability and exit rights: Before signing, confirm: if you decide to leave the platform, how is your data exported? In what format? Within what timeframe? At what cost? Vendors who make data portability difficult are creating exit barriers that reduce your negotiating position for every future contract renewal.

Third-party audit rights: Your institution must have the contractual right to request and review the vendor's SOC 2 report, penetration test results, and any relevant audit findings annually. This is an NCUA third-party risk management expectation, not an optional request.

Evaluation Red Flags: What to Watch for in Vendor Demos

Even with a complete requirements checklist, demo environments are designed to show capability in ideal conditions. Here are the questions that reveal what the platform actually does under real-world constraints:

"Show me an adverse action notice generated by your AI decisioning engine." If the output is a score range or a generic policy statement rather than specific, ECOA-compliant denial reasons, that is a compliance liability in production.

"Walk me through how we would update our underwriting policy for a new loan product without involving your development team." If the answer involves vendor support tickets, developer access, or a quarterly release cycle, your operations team has permanently lost control of their own underwriting rules.

"What does your core integration with [our specific core] actually do and what does it not do?" Integration depth varies significantly. Some vendors connect to the core for funding disbursement only; others synchronize member data, product parameters, and loan status bidirectionally in real time. The difference matters enormously for operational efficiency.

"Can you share your last 12 months of P1 incident data?" A vendor who cannot or will not share this is not yet operating at the transparency standard a regulated financial institution requires.

"What happens to our data on day one after contract termination?" The answer tells you everything about how the vendor thinks about your relationship.

How Algebrik One Is Built to Meet These Requirements

Algebrik AI built Algebrik One specifically because credit unions deserve a lending platform that was designed for their reality not adapted from a commercial bank product or patched from legacy architecture that predates smartphones.

Every requirement category in this checklist shaped how Algebrik One was built:

Functional depth: Algebrik One covers the full origination lifecycle - Digital Account Opening, Omnichannel Point of Sale, Lender's Cockpit, AI Decision Engine, and Portfolio Analytics in a single unified suite. There is no separate system for indirect lending, no manual handoff between POS and LOS.

Compliance architecture: Algebrik's partnership with Carleton integrates verified payment calculation and compliance APIs supporting 1,000+ calculation methods — including credit insurance, disability, and GAP across all consumer loan products. Adverse action outputs from the AI Decision Engine are designed to meet ECOA's specific-reasons standard.

Security posture: Algebrik operates as a cloud-native platform built on modern security infrastructure, with SOC 2 compliance as a foundational requirement rather than an afterthought.

Integration ecosystem: Algebrik's participation in the Jack Henry Vendor Integration Program and certified integration with Corelation's KeyStone core means credit unions connect to their existing infrastructure without bespoke engineering. The Scienaptic AI partnership brings advanced credit decisioning signals directly into the LOS workflow.

Implementation approach: Algebrik's implementation methodology is designed around credit union operational realities dedicated project management, sandbox configuration and validation, and parallel run support before live deployment.

Vendor accountability: Algebrik's model is built around ongoing partnership with credit unions, not a transactional relationship where support degrades after go-live.

Your Pre-Purchase Alignment Checklist: Internal Questions First

Before issuing an RFP or scheduling a demo, your team should be aligned on the answers to these internal questions because vendor evaluations surface answers to questions you have already asked yourself, not questions the vendor prompted.

- What are our current average cycle times by product, and what is our target?

- Which workflow steps account for the most manual labor and member friction today?

- Which loan products are we planning to add or expand in the next 24 months?

- What were the findings from our last NCUA examination related to lending?

- Do we have documented processes for adverse action notice generation and audit?

- How are we currently tracking fair lending data for monitoring?

- What is our current core system, and what integration method does our existing LOS use?

- What is our internal capacity for LOS configuration vs. what requires vendor involvement?

- What is our data migration and parallel run capacity?

- What is the total cost of ownership of our current system - including staff time, integration maintenance, and compliance remediation?

- What is the cost of member application abandonment at current conversion rates?

- What is the institutional risk exposure from our current compliance process?

When your team can answer these questions before the first vendor conversation, you negotiate from a position of clarity and you will not discover your requirements mid-implementation.

Frequently Asked Questions

What are the minimum requirements for a loan origination system at a credit union ?

The minimum functional requirements for a credit union LOS are: omnichannel digital application intake with cross-channel continuity, configurable automated underwriting, AI-powered credit decisioning with explainable outputs, real-time core system integration, automated ECOA-compliant adverse action notice generation, FCRA disclosure support, AML/KYC identity verification, document management with e-signature, calculation compliance across all loan product types, and role-based access with complete audit logging. A SOC 2 Type II security certification and a 99.9%+ uptime SLA are minimum vendor requirements.

What security certifications should a loan origination system have ?

What compliance capabilities must a loan origination system support for ECOA and adverse action ?

What is a sandbox-first LOS implementation and why is it better ?

What SLA and support standards should you require from an LOS vendor ?

Ready to get started?

More Blogs

Blog

Computerized Loan Origination: How Technology Transformed Lending

Blog

Consumer Finance Systems: Why Unified Platforms Win Over Fragmented Stacks

Blog

What are Loan Decisioning Softwares and Why Do they Matter?